In AI semiconductor design, the list of companies that make meaningful profit is still very short.

- NVIDIA and Google.

- Broadcom, Marvell, Qualcomm, MediaTek, and a small number of companies that build custom silicon for hyperscalers.

Everyone else is either squeezed somewhere inside that value chain, or still surviving on narrative and capital without a durable profit pool.

Most AI semiconductor companies are not producing operating profit.

At the same time, global AI semiconductor startup funding hit a record level in 2026.

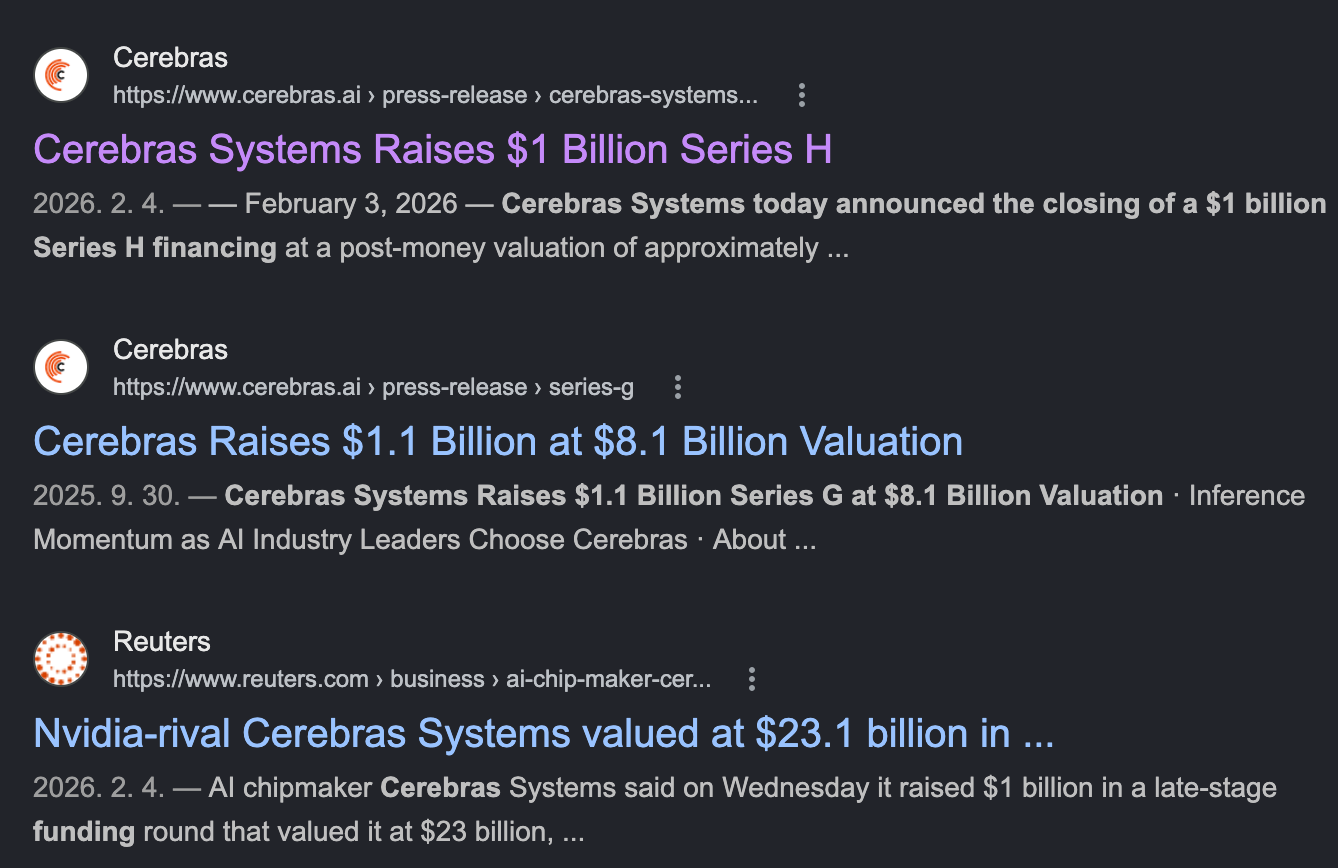

Cerebras raised $1B, Etched raised $500M, MatX raised $500M, Ayar Labs raised $500M, and d-Matrix raised $275M. Cambricon's market capitalization briefly approached $90B. Moore Threads jumped fivefold on the first day of its STAR Market listing. Global funding reached roughly $8.3B.

Revenue is missing, but capital keeps accelerating.

AI semiconductor investment continues, while the number of independently successful product companies remains close to zero. The useful question is not whether every startup wins. The useful question is which outcome bucket each company is moving toward.

Bull case 1: inference workloads are splitting apart

The strongest bull case is architectural. AI inference is no longer one homogeneous workload.

- Training favored large GPU clusters, NVLink or InfiniBand, and FP8 or FP16 throughput.

- Inference is fragmented: long-context prefill is compute-bound, decode is memory-bandwidth-bound, real-time speech needs ultra-low latency, recommendation uses sparse tensors, and edge inference has a different power envelope.

- When workloads fragment, specialized chips can beat general-purpose GPUs in a narrow but valuable domain.

In the inference era, the best custom chip can beat a general-purpose chip inside a clearly defined workload.

- Groq's LPU used SRAM-heavy deterministic dataflow to reduce token-generation latency.

- SambaNova's RDU pursued lower batch latency through reconfigurable dataflow.

- Cerebras compressed memory and compute distance inside one wafer-scale engine.

- Etched's Sohu gave up every architecture except transformers and marketed a transformer-only ASIC.

- d-Matrix used Digital In-Memory Compute to combine LPDDR and SRAM and avoid part of the GDDR or HBM cost curve.

- Lightmatter, Celestial AI, and Ayar Labs attacked the power cost of memory-compute interconnects through silicon photonics.

The theory is coherent. If the workload is specific enough, silicon specialization can create better economics. GPUs once separated graphics workloads from CPUs. A similar separation can happen inside inference.

Bull case 2: sovereign AI creates a new demand category

The second bull case is sovereign AI. AI infrastructure is becoming a strategic asset for services, defense, industry, public data, and national security.

- Most leading AI accelerators still come from the United States.

- Free trade is no longer the default semiconductor regime.

- Export controls, tariffs, sanctions, and national security policy now shape sourcing decisions.

That means non-US governments want alternatives. UAE, Saudi Arabia, the EU, Japan, Korea, India, Indonesia, and Malaysia are all spending billions to build domestic or trusted AI infrastructure.

These buyers do not only optimize for price. They optimize for supply diversity, political safety, data sovereignty, and local industrial policy. In that market, NVIDIA's technical lead is not the only variable.

- Qatar Investment Authority and Temasek participated in d-Matrix's Series C.

- Saudi Aramco appears on Rebellions' cap table.

- The positioning is clear: many startups are selling national AI optionality, not only chips.

The more export controls and tariff pressure rise, the more room appears in markets that NVIDIA cannot fully serve.

China: the forced-separation market

China is the most extreme form of sovereign AI. US export controls pushed NVIDIA's share in China's data-center AI chip market down from an estimated 95% toward the floor, and Cambricon, Moore Threads, MetaX, Biren, and Huawei HiSilicon moved into the gap.

Cambricon's 2025 revenue grew roughly fourteenfold year over year and the company reported its first quarterly profit. Large ByteDance orders helped drive the shift.

- Cambricon targets 500,000 AI chip shipments in 2026.

- Moore Threads passed STAR Market IPO review in 88 days and listed on December 5.

- MetaX listed two weeks later.

- Biren moved ahead with a Hong Kong listing in early 2026.

Jensen Huang and securities analysts increasingly view China as a market that can satisfy most domestic AI chip demand through domestic suppliers.

This is not pure product-market fit. It is political demand redistribution. But the outcome is still real: Chinese AI chip companies gained revenue growth and access to capital markets by dominating a forced-separated domestic market.

Bull case 3: capital-market fit can replace product-market fit

The third bull case is cynical, but practical. Many AI semiconductor startups are funded by capital-market fit before they prove product-market fit.

- If the narrative remains strong, valuation can survive delayed revenue.

- If valuation survives, the next round can arrive.

- If enough large rounds accumulate, the company can reach IPO or become an acquisition target.

FuriosaAI's decision to reject Meta's reported $800M offer and pursue an IPO fits this logic. Groq had little meaningful product revenue before being acquired by NVIDIA for $20B, nearly 100 times the cumulative funding base of roughly $210M.

Etched is an even cleaner example. Two Harvard dropouts founded the company in 2022. By March 2026, it had not shipped customer chips, but had raised more than $625M and reached a $5B valuation. The bet was not on audited revenue. It was on the thesis that transformers would dominate for another five to ten years.

Cerebras could pursue an IPO because the market wanted a liquid alternative to NVIDIA. Bulls expect this cycle to continue for at least five to seven years because hyperscaler AI capex is moving toward hundreds of billions of dollars per year.

Bear case 1: what are these companies actually selling?

The bear case begins with a simple question. Are these companies making real money?

- Cerebras generated meaningful 2025 revenue, but about 86% came from two sovereign customers: G42 and MBZUAI in the UAE.

- SambaNova's 2024 revenue was reportedly below $100M, and the mix leaned toward service revenue rather than pure system sales.

- Groq had little meaningful product revenue before NVIDIA acquired it.

- Etched had not shipped chips as of March 2026.

- d-Matrix began sampling Corsair in 2025, but revenue scale is still undisclosed despite a $2B Series C valuation.

- Korean NPU companies remain mostly in proof-of-concept revenue. Chinese companies have revenue, but much of it comes from a politically separated domestic market.

The largest potential customers are hyperscalers and large enterprises. But the cost of moving from NVIDIA to a specialized chip is not a simple bill-of-materials comparison.

Customers must rewrite or validate model code, operating infrastructure, monitoring tools, developer workflows, regression tests, and debugging paths built on CUDA. Only a few hyperscalers have software teams large enough to absorb that switch.

- Those hyperscalers usually do not buy NPU startup chips.

- They ask Broadcom or Marvell to design internal ASICs.

- Google TPU, Amazon Trainium and Inferentia, Meta MTIA, and Microsoft Maia all followed that path.

The remaining markets are sovereign AI, tier-2 cloud providers, large enterprise on-prem deployments, edge or embedded devices, and acquisition outcomes. Combined, that is much smaller than NVIDIA's data-center revenue pool.

Bear case 2: NVIDIA attacks inference directly

The biggest blow to the specialist thesis is NVIDIA's 2025 to 2026 inference roadmap. The old argument was that NVIDIA GPUs were built for training and therefore inefficient for inference. That argument is being dismantled.

NVIDIA is explicitly designing silicon for agentic AI and advanced reasoning. Rubin CPX is a separate GPU aimed at long-context inference.

- 30 petaFLOPs of NVFP4 compute.

- 128GB of GDDR7 memory instead of HBM.

- The choice of GDDR7 matters because the prefill phase needs large memory capacity more than ultra-high bandwidth.

- The Vera Rubin NVL144 CPX rack combines 8 exaflops of performance with 100TB of fast memory.

- Hardware video encode and decode are integrated into the monolithic die.

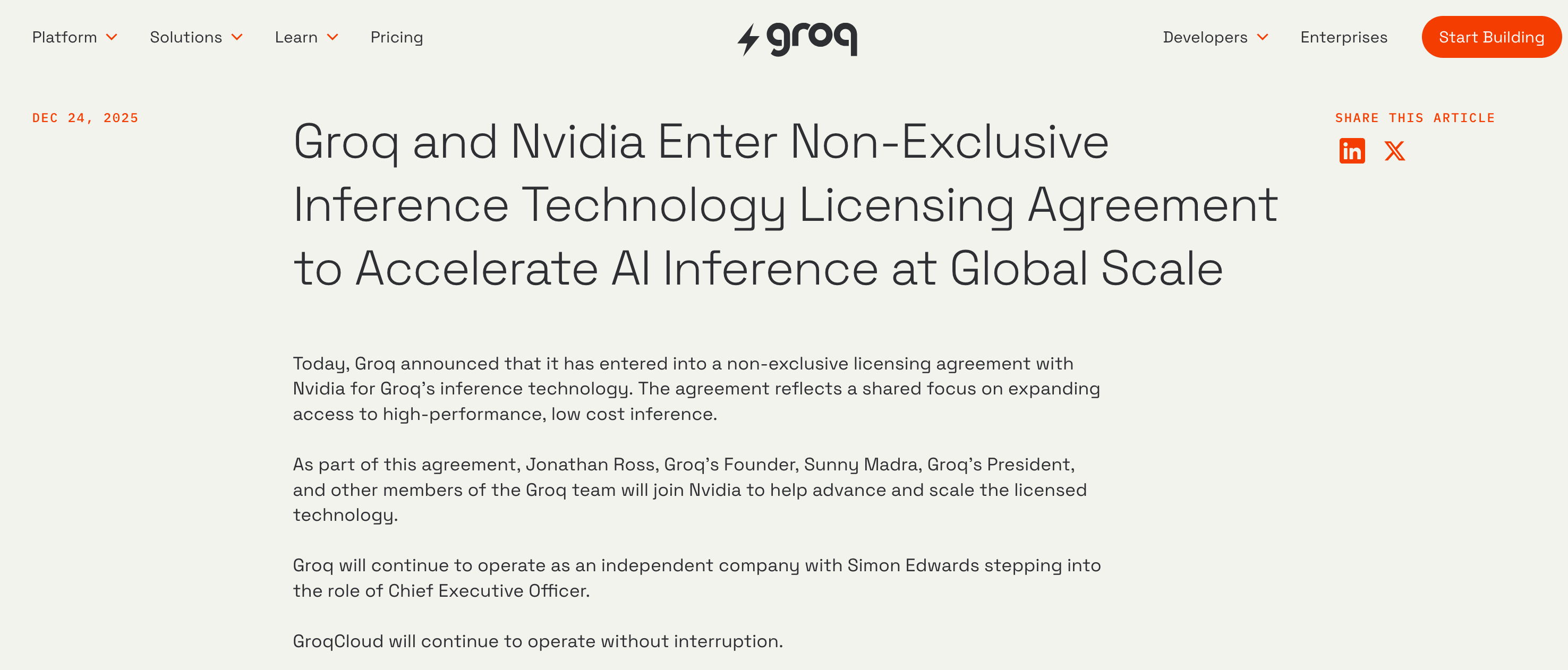

The LPX path tightens the pressure further. NVIDIA acquired Groq and can integrate LPU-style low-latency inference into its own rack architecture. By GTC 2026, the 256 LPU per rack configuration directly targeted low-batch, ultra-low-latency inference.

Startups were built around the message that inference-specific chips would beat GPUs. NVIDIA answered by buying Groq and attaching CUDA, NVLink, and rack-scale distribution to that idea.

Bear case 3: hyperscaler in-house silicon

The competitive map is even harsher because pressure comes from four directions at the same time.

- NVIDIA is entering specialist inference SKUs through Rubin CPX and LPX.

- Broadcom and Marvell effectively dominate the hyperscaler ASIC market.

- Google TPU, Meta MTIA, Microsoft Maia, OpenAI custom silicon rumors, ByteDance, and Apple all point toward in-house silicon.

- Qualcomm is entering data-center inference with mobile power-efficiency DNA, while AMD attacks inference with MI400 and absorbed Untether AI talent.

That leaves a narrow space for independent specialists. Cerebras moved toward sovereign customers. Groq moved into NVIDIA. Untether moved to AMD. Celestial AI moved to Marvell. Graphcore moved to SoftBank.

For Etched, d-Matrix, Tenstorrent, Lightmatter, SambaNova, MatX, and many Korean and Chinese NPU companies, the real question is how long capital can bridge the gap before revenue arrives.

Future outcomes: where do AI semiconductor startups go?

Group 1: M&A

- Groq to NVIDIA, Celestial AI to Marvell, Untether to AMD, Graphcore to SoftBank.

- The independent product-company path is abandoned before capital runs out.

- Founders and early investors exit. IP and talent are absorbed into the incumbent product line.

Group 2: sovereign AI

- Cerebras, some Korean NPUs, and some Middle East-backed companies fit here.

- Revenue concentrates in a few sovereign customers, so the company's fate depends on political commitment.

- These companies may not become global champions, but they can become viable national infrastructure vendors.

Group 3: state-backed national champions

- Chinese AI chip companies and some Korean NPU companies fit this bucket.

- The state supplies capital, creates customer demand, and makes failure politically costly.

- Cambricon's revenue surge is not just product-market fit. It is the result of demand being redistributed by geopolitical separation.

Group 4: independent product companies

- Etched, d-Matrix, Tenstorrent, Lightmatter, SambaNova, MatX, and parts of Cerebras.

- This is the hardest route. Without hyperscaler adoption, revenue is weak. With hyperscaler adoption, the company becomes an acquisition target.

- The desire to stay independent increases capital intensity.

Group 5: IP licensing pivots

- Tenstorrent is the most visible case.

- Instead of only selling chips, it licenses RISC-V CPU IP and Tensix AI cores to LG, Hyundai, Samsung, Bosch, and others.

- This model avoids direct customer-acquisition battles, foundry allocation fights, and can produce software-like margins through license plus royalty economics.

- The tradeoff is valuation reset. IP licensing multiples are usually lower than product-chip multiples, and royalty revenue takes years to accumulate.

Group 6: edge AI, on-device AI, and AIoT

- Hailo, SiMa.ai, Axelera, Ambarella, Mobilint, and parts of DeepX belong here.

- The market is smaller than the data center, but more fragmented and less exposed to a single hyperscaler customer.

- Margins are lower, but supply-chain risk and direct NVIDIA pressure are also lower.

Conclusion

The fate of AI semiconductor startups is not decided only by the skill of semiconductor engineers.

It is decided by capital structure, HBM access, foundry slots, customer contracts, political alignment, software ecosystems, and exit pressure.

Insiders already understand the mismatch. A VC-backed company promises a high-multiple exit. To protect that multiple, it must look like a product company. To look like a product company, it builds an SoC. Once it builds an SoC, pivoting to IP licensing becomes structurally difficult.

A state-backed company promises a national exchange listing and industrial-policy proof. That also pushes it toward SoCs, sovereign customers, and narrative-driven valuation.

Founders rarely say this publicly because fundraising requires the simpler story: our chip is better than NVIDIA for this workload.

That frame mismatch explains the industry. Billions of dollars enter specialist startups every year, but very few global champions emerge.

That does not mean the money disappears. Capital is recycled, founders move toward exits, technology is commercialized through incumbents, and talent is redistributed across the semiconductor ecosystem.