TL;DR

- Trump's Q1 2026 OGE filing showed 3,711 trades over 11 weeks, with an estimated transaction range around $490M. That is an extraordinary level of securities activity for a sitting president.

- The book sold roughly $60M of MSFT, AMZN, and META, while buying NVIDIA, Synopsys, Cadence, Broadcom, Lam Research, and Dell. This is not a single-stock bet. It maps across eight layers of the AI infrastructure value chain.

- The optimistic read: EDA tools, equipment, chips, servers, cooling, and power are all represented. The skeptical read: Bloomberg analysis suggests much of the activity may reflect automated execution, tax-loss harvesting, and index rebalancing rather than deliberate stock picking.

- The biggest missing pieces are HBM and foundry. There is no position in SK Hynix or Samsung Electronics, only a small Micron buy, and no TSMC position despite TSMC passing through most of the value chain.

Trade scale and timing

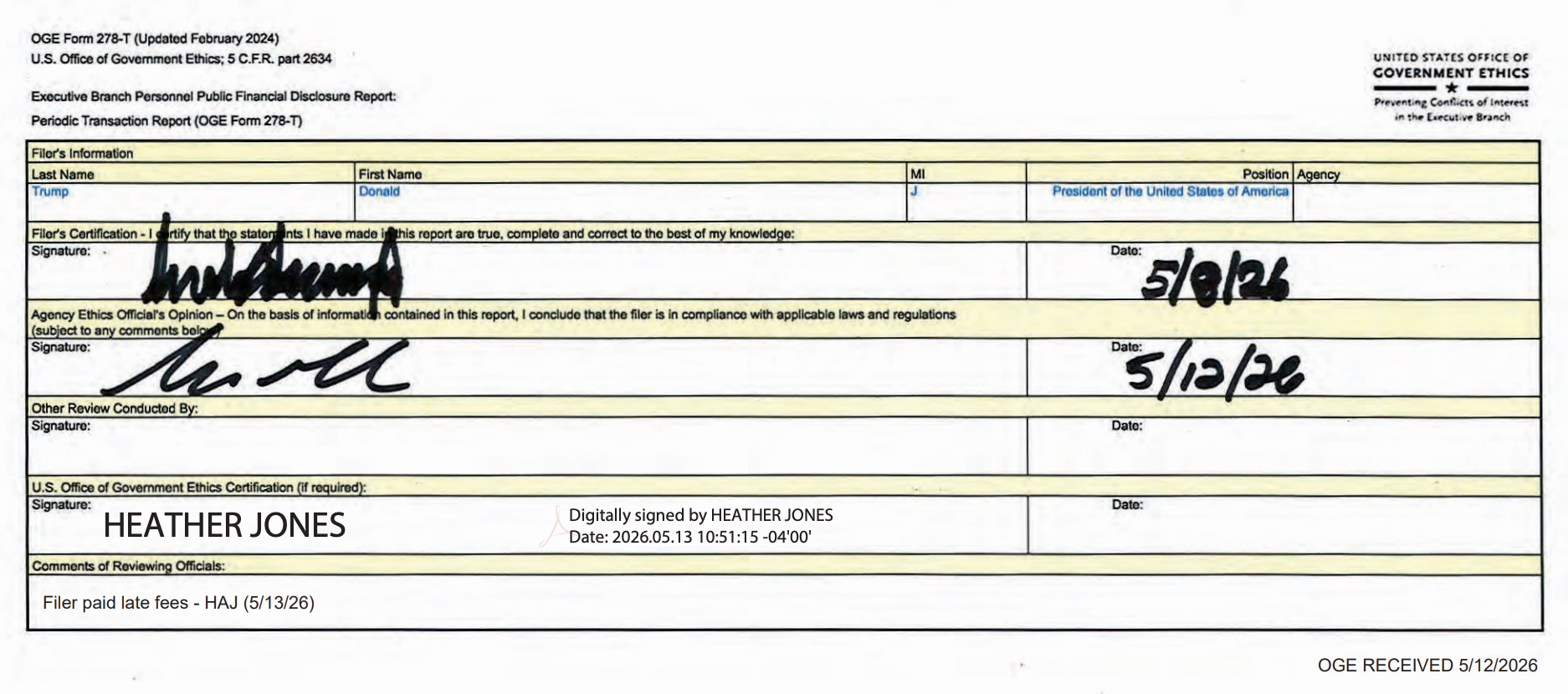

- Total trades: 3,711 trades, including 2,196 purchases and 1,014 sales. Of these, 3,642 were equity trades. Two OGE Form 278-T filings were filed on May 12, 2026.

- Estimated transaction value: $220M-$750M according to Reuters, with a midpoint near $490M.

- Period: January 6 to March 30, 2026, roughly 11 weeks, certified after a late-fee payment.

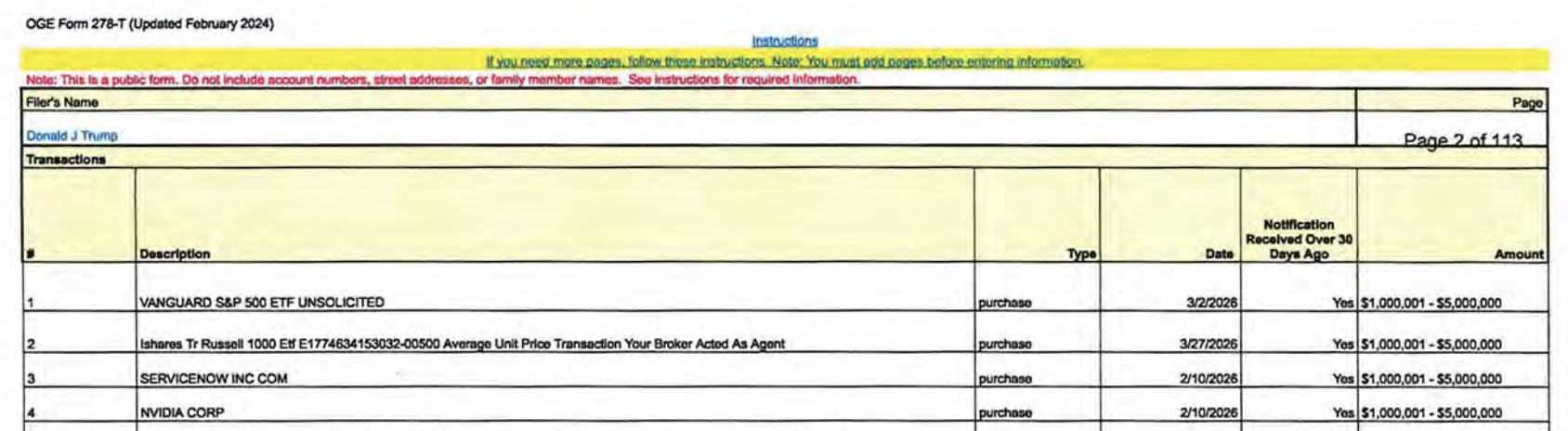

- February 10 rotation: MSFT, AMZN, and META were sold in $5M-$25M ranges each, totaling roughly $60M. On the same day, purchases concentrated in NVDA, Synopsys, Cadence, and Adobe.

- March surge: more than 2,000 trades were concentrated in March after escalation around Trump's Iran military operation.

Because the disclosure uses value ranges, the exact dollar amount cannot be reconstructed precisely.

Trump's portfolio rotated from Big Tech toward AI infrastructure.

Bloomberg and Fortune analysis suggests that a large portion of the 3,711 trades may have come from automated execution, tax-loss harvesting, and index rebalancing. There is no hard evidence that Trump personally selected each security. The Trump Organization has said the portfolio is managed by an independent third-party institution.

A: What Trump bought: eight layers of the semiconductor value chain

1. EDA tools

- Synopsys (SNPS): six buys versus two sells. Ticket ranges are undisclosed, but an EDA software allocation of $3M+ is plausible within the portfolio.

- Cadence (CDNS): seven buys, with midpoint estimates around $3M. Together with Synopsys, this completes the EDA duopoly exposure.

Synopsys and Cadence together control more than 70% of the EDA market. Switching cost is extreme. A 3nm chip program cannot realistically start without this toolchain.

After the US Bureau of Industry and Security restricted advanced EDA exports to China in 2025, Synopsys and Cadence became more than software companies. They became national-security assets. The EDA allocation reflects that reality.

- EDA depends on real semiconductor design data, which is not publicly available. That makes the field difficult for generic AI hyperscalers to attack directly.

- As inference becomes more important than training, the custom ASIC era becomes more important.

- More custom chips imply more design activity and more EDA usage.

- The risk: Synopsys' GAAP profit fell after the Ansys acquisition, Cadence's EPS fell after the Hexagon acquisition, and China export restrictions remain a large revenue headwind.

2. Semiconductor equipment and materials

- Lam Research (LRCX): five buys, no sells. Lam is the leading etch-equipment player. High-aspect-ratio etch determines yield in 3D NAND layer stacking, and TSMC N2 plus Samsung 2nm GAA both rely heavily on advanced etch tools.

- Linde (LIN): three buys, no sells. Linde is a global leader in ultra-high-purity gases such as He, Ne, and Ar for semiconductor fabs. EUV lithography throughput is highly sensitive to neon purity.

3. AI chips

- NVIDIA (NVDA): seven split purchases. The largest ticket was in the $5M-$25M range, and the remaining six were in the $1M-$5M range. Midpoint exposure is roughly $11M-$15M.

- Broadcom (AVGO): one $1M-$5M ticket. Broadcom is the custom ASIC and networking-switch layer behind Google TPU, Meta MTIA, and other hyperscaler silicon programs.

- AMD: four buys versus four small sells, net buyer. MI400 gives AMD a second-half 2026 path into the AI GPU market.

NVDA is the general-purpose AI accelerator. AVGO is the hyperscaler custom ASIC layer. If inference overtakes training, the portfolio can survive through either path.

TheStreet argued that the Broadcom buy came just before Trump mentioned Broadcom in a speech about reviving American semiconductor manufacturing. 24/7 Wall St reported that shortly after an NVDA purchase, Trump signed an executive action to accelerate AI chip export approvals.

4. AI servers

- Super Micro Computer (SMCI): four buys, one small sell. SMCI is a direct liquid cooling server player and a key NVDA GB300 rack integration partner.

- Dell Technologies (DELL): three buys, no sells. Dell captures enterprise AI server and traditional data-center refresh demand.

5. Interconnect

- Amphenol (APH): three buys, no sells. Amphenol is a high-speed interconnect leader across NVLink backplanes, PCIe Gen 6 lanes, and dense connector systems.

6. Data-center cooling

- Lennox (LII): three buys, no sells. Commercial HVAC becomes structurally more important as GPU clusters move toward 50-100kW per rack and liquid cooling.

7. Power management

- Eaton (ETN): four buys, midpoint estimate around $3.28M. Eaton supplies data-center power distribution, UPS, and switchgear. AI data-center power density is doubling every few years.

8. Cloud infrastructure

- Oracle (ORCL): eleven split purchases, midpoint estimate around $3.62M. Oracle is a Stargate cloud partner and is building OCI GPU clusters for LLM training.

Allocation summary

On midpoint estimates, total semiconductor and AI infrastructure exposure exceeds $50M, roughly 35-40% of total equity-portfolio activity.

B: What Trump missed: HBM and foundry

If this book is truly a strategic AI infrastructure bet, the largest holes are clear.

1. HBM: the biggest 2026 bottleneck is almost absent

- SK Hynix: HBM3E 12-high production, estimated 50%+ HBM market share in 2025, and major GB300 HBM supplier. Trump portfolio: no position.

- Samsung Electronics: HBM3E approval complete, HBM4 mass-production target in 2026 H2, and a key diversification candidate for NVIDIA. Trump portfolio: no position.

- Micron (MU): HBM3E 8-high production and HBM4 roadmap. Trump portfolio: small buy, but far smaller than NVDA exposure.

This is a major gap. Each NVDA GPU uses multiple HBM stacks. As GPU capex rises beyond $280B, HBM demand can grow even faster because GB300 increases HBM capacity per GPU versus GB200.

The book owns GPUs, servers, cooling, and power, but has only a small position in the most expensive component inside the GPU package.

2. TSMC: six layers of the value chain pass through it, but there is no position

TSMC (TSM) is the company that actually manufactures chips for NVDA, AMD, Broadcom, and many SMCI-linked systems. Six of the eight layers pass through TSMC advanced packaging and process capacity. TSMC ADR is listed on NYSE and would be visible in the OGE filing. It is not in the book.

The irony is obvious. Trump approved CHIPS Act support for TSMC's Arizona fab and framed domestic semiconductor manufacturing as a national-security issue, but the portfolio did not buy TSMC.

There is Intel exposure in the book, but Intel Foundry has not yet demonstrated comparable advanced-node production momentum.

Implication for the semiconductor industry

CHIPS Act subsidies, semiconductor-equipment export controls, and AI chip export restrictions all sit close to policy decisions made by the same person whose personal portfolio has exposure across the AI semiconductor value chain.

If the president is a shareholder in Synopsys, Cadence, NVIDIA, Broadcom, TXN, Dell, Intel, and Micron, how should the industry price the probability of export-control relaxation?