electronic design automation (EDA) and semiconductor IP sectors have been recognized for their high growth and strategic importance in the AI era.

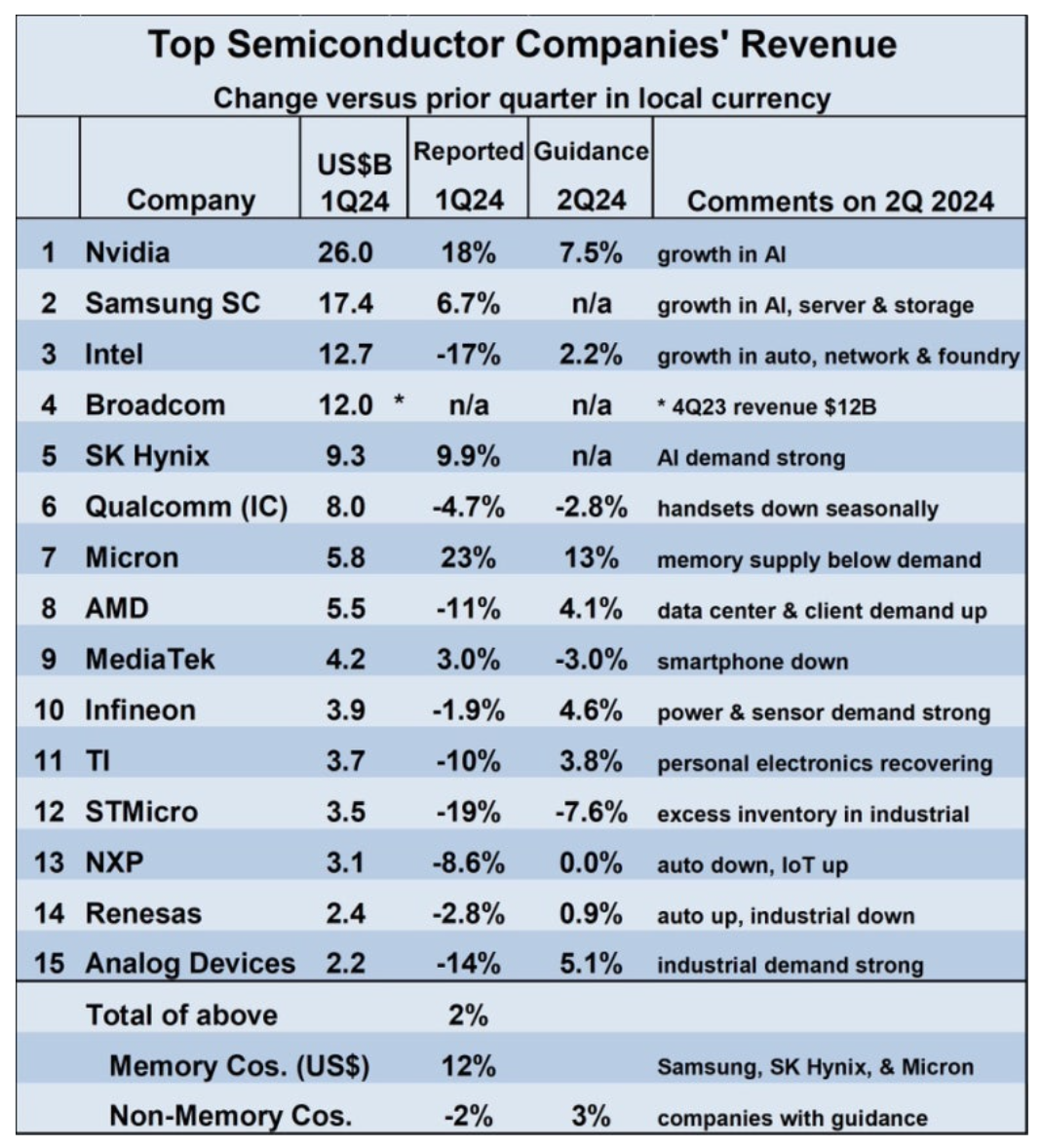

Big techs are doing well, but certain semiconductor companies are still facing challenges.

These are the companies that used to be the best in the world and are now struggling very badly.

These companies are now reducing their operating activities, financing activities, which means they are not hiring, they are reducing their staff, and they are reducing their investments.

These companies used to have world-class products, and they used to spend a lot of money on EDA, but in the next few years, they are going to reduce their spending significantly.

Vendor companies are facing uncertainty.

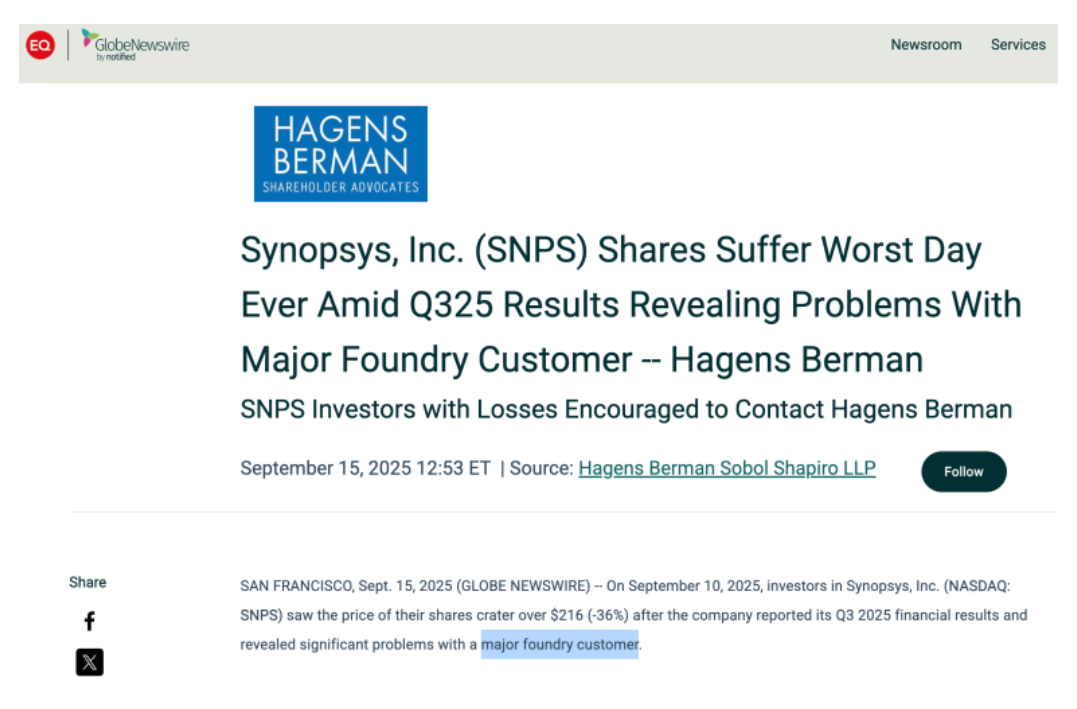

In September 2025, Synopsys, Cadence, and others saw their stock prices drop by more than -tens of percent in a single day after reporting quarterly results.

The EDA industry has grown, but the IP business is reportedly struggling, with major customers losing contracts and operating margins shrinking.

Here are some scenarios of what might happen:

- Cadence is moving into adjacent areas with its "Intelligent System Design" strategy,

- Synopsys recently acquired physics simulation software company Ansys to build a portfolio that spans from chip design to multi-physics simulation.

- intel was the world's leading semiconductor company until a few years ago.

- Intel has been contracting a lot of EDA/IP to different EDA companies (especially Synopsys)

- Intel is not doing well and is shrinking its business.

- Synopsys brings strengths in logic synthesis, physical design, IP cores, signoff, and verification,

- Cadence brings strengths in analog/mixed-signal design, PCB/package tools, and digital place and route (P&R).

- Synopsys - Ansys integration performance:

- With the acquisition of Ansys, which closed in September 2025, Synopsys added a world-class physics simulation tool to its portfolio. Ansys has a strong customer base in non-semiconductor sectors, including aerospace, automotive, defense, and industrial devices.

- Synopsys can double its customer base by cross-selling its existing semiconductor design customers with Ansys' engineering software customers. In particular, semiconductors for autonomous and electric vehicles are not only about the performance of the chip itself, but also about its thermal/mechanical reliability, and the Synopsys-Ansys combined solution is ideal for this system-level design.

- In the medium term, the acquisition of Ansys is not only immediately accretive to Synopsys revenue (Ansys is estimated to be around $2 billion in annual revenue), but also geographically more European revenue (Ansys has many European customers) and product-wise diversifying. This reduces our dependence on Intel or specific fabless customers.

- Growth in automotive and industrial semiconductors:

- The electric vehicle (EV) era is driving an explosion of semiconductor content in vehicles. AI chips and high-speed SoCs are being used in advanced driver assistance (ADAS), autonomous driving, vehicle communications, and more, and the demand for these automotive chip designs is skyrocketing.

- EDA companies have been preparing early for automotive safety certifications (IP and tools) and automotive design references with foundries such as TSMC. As a result, many automotive semiconductor designers are adopting EDA and IP.

- As mass production of automotive 7nm/5nm chips ramps up over the next year or two, EDA-related revenue is expected to rise proportionally.

- In addition, high-reliability system semiconductors, such as chips for industrial IoT and 5G infrastructure, are also targeted by EDA. This new demand could more than compensate for the decline in sales in traditional areas such as Intel and PC/mobile.

- Expansion of chiplet and system-level design:

- The semiconductor industry is adopting chiplet architecture and 3D additive technologies to overcome the integration limitations of a single die. Enabling these changes requires system-level design and verification tools.

- EDA companies already have tool sets for 3DIC design and are leading IP development by participating in the UCIe consortium, the leading chiplet connectivity standard.

- Disparate chips are increasingly being integrated at the package level, especially in data center CPUs, AI accelerators, and more, creating a multidie design software market.

- EDA executives call this the "Silicon to Systems" opportunity and see it as a future growth driver for the company.

- If we see early revenue wins in this area, it would not only replace what Intel has lost, but it would open up a whole new market for EDA.

- Cloud-based small and medium-sized customer expansion:

- Numerous fabless startups founded in the AI boom are getting early access to tools through EDA companies' cloud EDA platforms.

- Synopsys reported that in 2023 alone, it had more than 100 startup customers in the cloud. While some of these will die off as competition increases, the winners could become the next big customers.

- For example, when the top AI chip startups start developing chips with tens of billions of dollars in investment, Synopsys EDA usage and revenue will increase significantly.

- In other words, the "next Nvidia" or "next Mobileye" could be a new core customer for Synopsys if it comes to fruition, and having a head start on this potential customer pool bodes well for Synopsys going forward.

Scenario A: A major customer abandons or reduces its EDA and IP contracts altogether.In conclusion, we believe that EDA companies face volatility risk related to existing customers in the short term, but have growth potential in the long term due to product portfolio diversification and demand for AI and next-generation semiconductors.

Background: EDA industry trends

The global EDA industry is experiencing steady growth, driven by increasing semiconductor design complexity and the AI chip design craze.

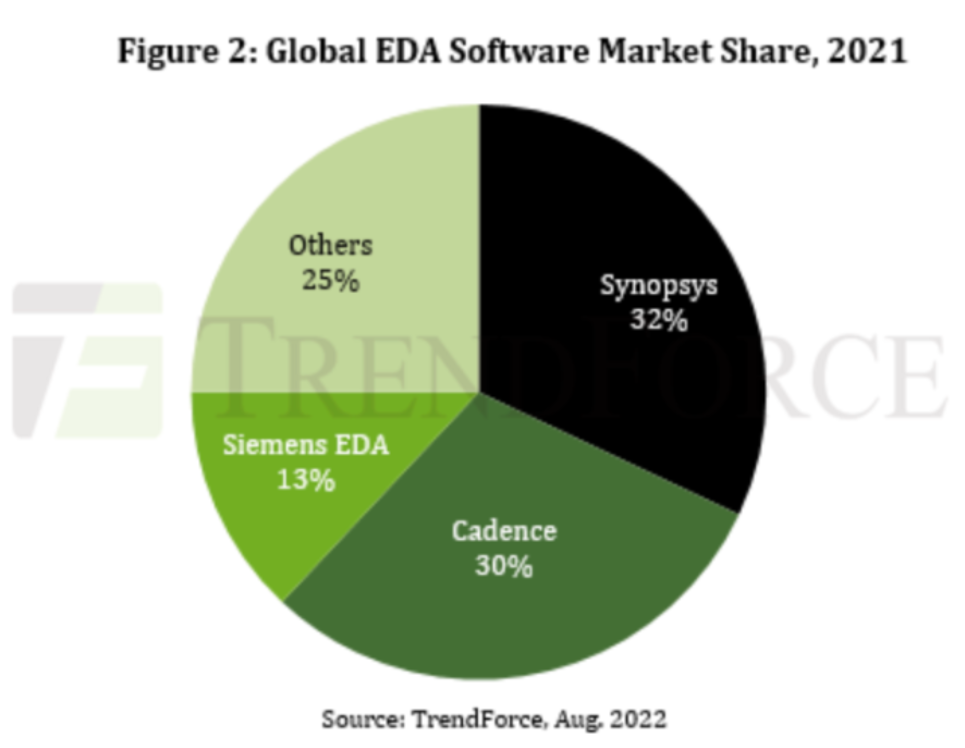

The industry structure is highly concentrated, with Synopsys and Cadence in the U.S. accounting for more than half of the market share and Siemens EDA (acquired by Mentor Graphics) accounting for about 13% as of 2021, forming a Big3 EDA landscape.

The top three or four EDA companies control more than 70% of the global market, with Synopsys maintaining its position as the #1 EDA company by revenue.EDA tools need to continue to innovate to keep pace with the entry of semiconductor microfabrication and the trend of utilizing AI in chip design.Major players such as Synopsys and Cadence are reinvesting in R&D to develop the latest design tools, and are incorporating AI-based automation capabilities into their design software to reduce design time and increase workforce productivity. (While Synopsys has higher revenue, Cadence has higher revenue per employee.)In particular, Synopsys is using its Synopsys.AI platform, which applies reinforcement learning and generative AI to design optimization, and Cadence is advancing similar AI-assisted design capabilities.

또 다른 블루오션: Digitial Twin with EDA

Emulators for Hardware Verification and Virtual Prototype, once ancillary products that have now grown to over $1B and become new revenue streams for EDA companies.

Silicon to System

EDA companies are expanding beyond simple chip design tools into System-level engineering software.

We want to be a company that can do all science and engineering simulations, not just semiconductor simulations.

The move is interpreted as a strategy to address the demand for system-level design in automotive, aerospace, and other industries, and to broaden its market to the total engineering ecosystem. However, the consensus is that Synopsys paid too much for Ansys.

Synopsys and Cadence don't just want to be the No. 1 EDA company; they want to be the top U.S. stock.

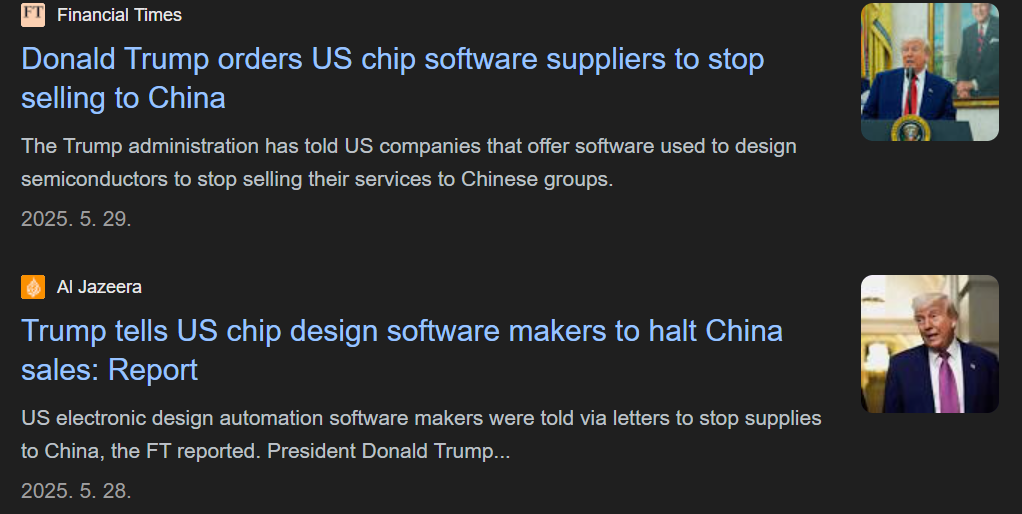

Geopolitical issues

Recent geopolitical issues have also impacted the EDA industry. Recent U.S. government export controls to the People's Republic of China temporarily restricted Synopsys and Cadence from doing business in the country, but they have resumed supporting Chinese customers when the restrictions are eased in 2025.

China is an important market, accounting for more than 10% of global EDA revenue, so there is demand volatility due to regulatory changes.

The Chinese government is also encouraging the development of indigenous EDA software, so the emergence of Chinese indigenous EDA companies could be a competitive factor for global players in the long term.

However, in the advanced process EDA space, technology barriers are high, which will likely keep Synopsys and others dominant for the foreseeable future.

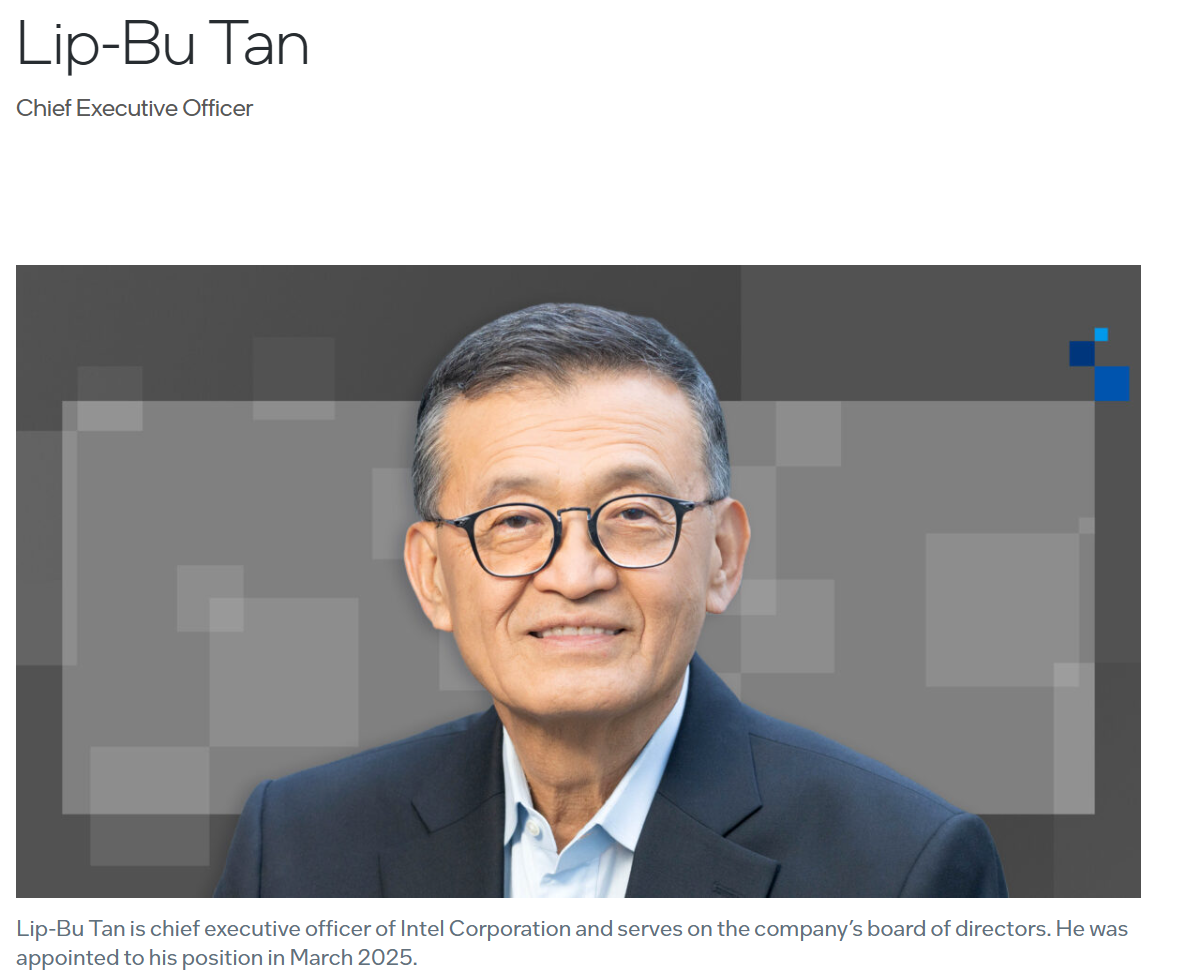

Intel–NVIDIA 협력, New Intel CEO Lip-Bu Tan, formerly of Cadence

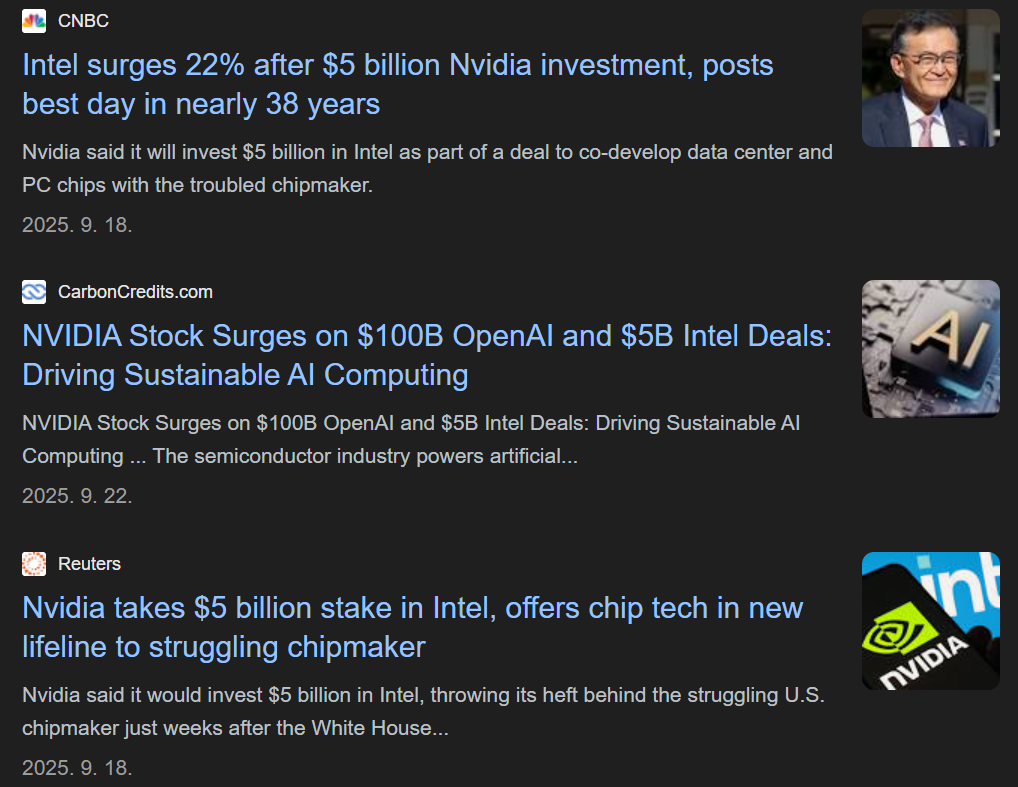

One of the most closely watched events in the semiconductor industry in 2025 was the Intel-NVIDIA strategic collaboration announcement.

In September 2025, NVIDIA announced that it would acquire a stake in Intel for approximately $500 million, and that it and Intel would co-develop future chips for data centers and PCs.

In this collaboration, Intel will design its own x86 CPUs and jointly develop an integrated AI superchip connected by a high-speed interconnect (NVLink) with NVIDIA's GPUs.

NVIDIA's investment immediately boosted Intel's stock, with industry observers calling it "Intel's tie-up with NVIDIA to survive in the AI era."At the same time, the collaboration is also seen as a source of tension for competitors such as AMD and TSMC, as Intel has EDA, IP, and foundries.The implications for EDA are both positive and negative.

Nvidia-Intel: What's in it for the EDA company

If NVIDIA's support increases Intel's financial stability and the sustainability of its foundry business, it could make it less likely that Intel will break its EDA/IP deal with Synopsys.If the NVIDIA infusion eases the pressure on Intel to slash design tool budgets, it could be the best of both worlds for the companies that supply Intel with EDA and IP.There is also plenty of room for EDA tools and IP to be utilized in the next generation of Intel-NVIDIA co-developed chips.For example, we could see Synopsys supplying the high-speed SerDes IP or PCIe controller IP needed for NVLink interconnects.

Nvidia-Intel: What's at stake for the EDA company

The background and strategy changes of Lip-Bu Tan, Intel's new CEO. Lip-Bu Tan is an EDA industry titan who was CEO of Cadence Design Systems from 2009-2021 before taking over as Intel CEO in March 2025.Whether the NVIDIA-Intel deal will increase the total demand for EDA/IP remains to be seen.His appointment is a sign that Intel values the semiconductor design ecosystem and brings EDA expertise to the table, but at the same time, if Lip Butan can use his relationships with Cadence management to get a better deal, it could be a bit more painful for Synopsys.In reality, the contract battle between Synopsys and Cadence is pretty tight, and if a particular tool is a bit lacking technically, they attack on price.In addition, Lip-Bu Tan grew Cadence during his time at Cadence by leading the industry's M&A and new business expansion, so it's possible that Intel is also looking to internalize design capabilities, either through developing its own EDA tools or through acquiring third parties.To recap,For Synopsys investors, there are two opposing possibilities:1. The risk of losing long-term contracts if Intel fails2. The risk that even if Intel succeeds, it will give Carence, not Synopsys, a chance

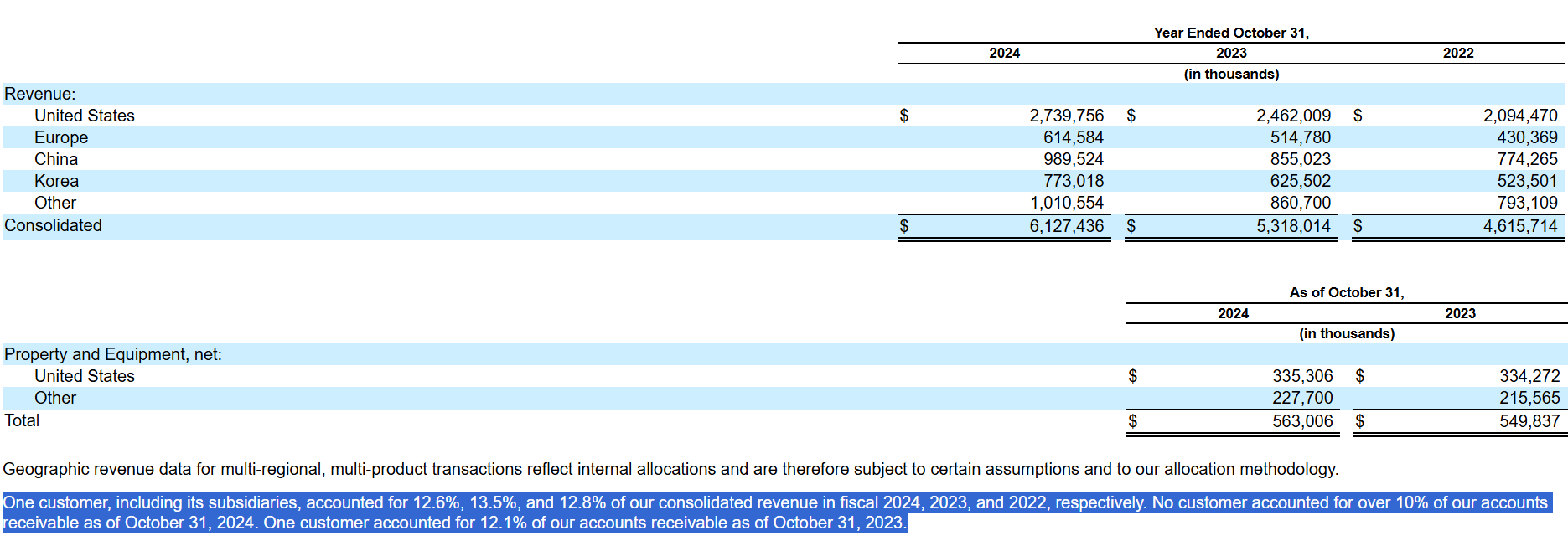

Synopsys has a high customer concentration, with about 12.6% of its $6.1 billion in 2024 revenue coming from a single customer.

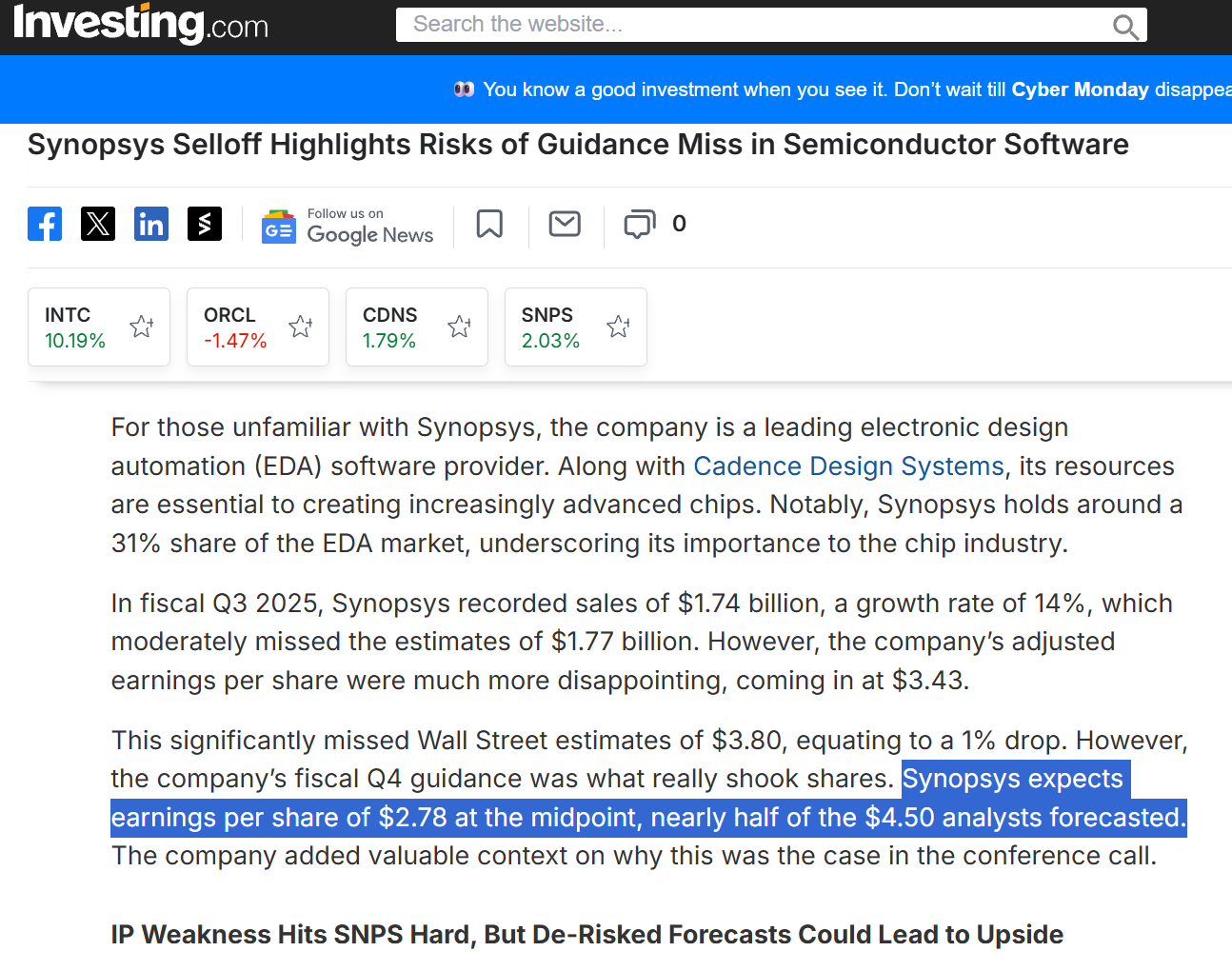

Synopsys fell more than $120 million short of expectations in the quarter, with Design IP division revenue declining -7.7%, and management acknowledged that "anticipated IP deals did not close due to difficulties with a major foundry customer."

In addition, U.S. mass export restrictions also disrupted sales in China, adding to the IP slump."Our IP business did not meet our expectations," said Synopsys CEO Sassine Ghazi, explaining that:1) new export regulations delayed design starts in China,2) a major foundry customer slowdown had a significant impact on our full-year results,3) some of our roadmap/resource allocation decisions did not deliver the intended results,"Synopsys CEO Sassine Ghazi said.In the immediate aftermath of this announcement, Synopsys shares plunged -36% in a single day, the company's worst single-day drop since its initial public offering.

The bigger shocker was that Synopsys guided EPS for the fourth quarter of 2025 40% below its previous guidance.

Synopsys is perceived as a stable company that has been cash cow for decades, so the guidance was taken as a warning sign by investors.

Investors have begun to reassess Synopsys' mid- to long-term growth story in the wake of this event:1. While the AI boom is driving strong demand across the EDA industry, it raises questions about how resilient Synopsys' earnings can be to external shocks, such as the post-crash cleanup of AI chip startups or major customer budget cuts.2. The fate of Intel-related revenue, in particular, will be a key factor in Synopsys' earnings volatility and stock price reassessment over the next year or two.3. To resolve investor-management tensions, Synopsys will need to complement its growth story with customer diversification and new market expansion and a more transparent risk disclosure.

Competitive Landscape

The EDA market is effectively a Synopsys and Cadence duopoly.

The two companies have been complementary competitors in terms of their product portfolios:Intel sales are down, but other new sales are bigger, so the overall picture could be one of growth.