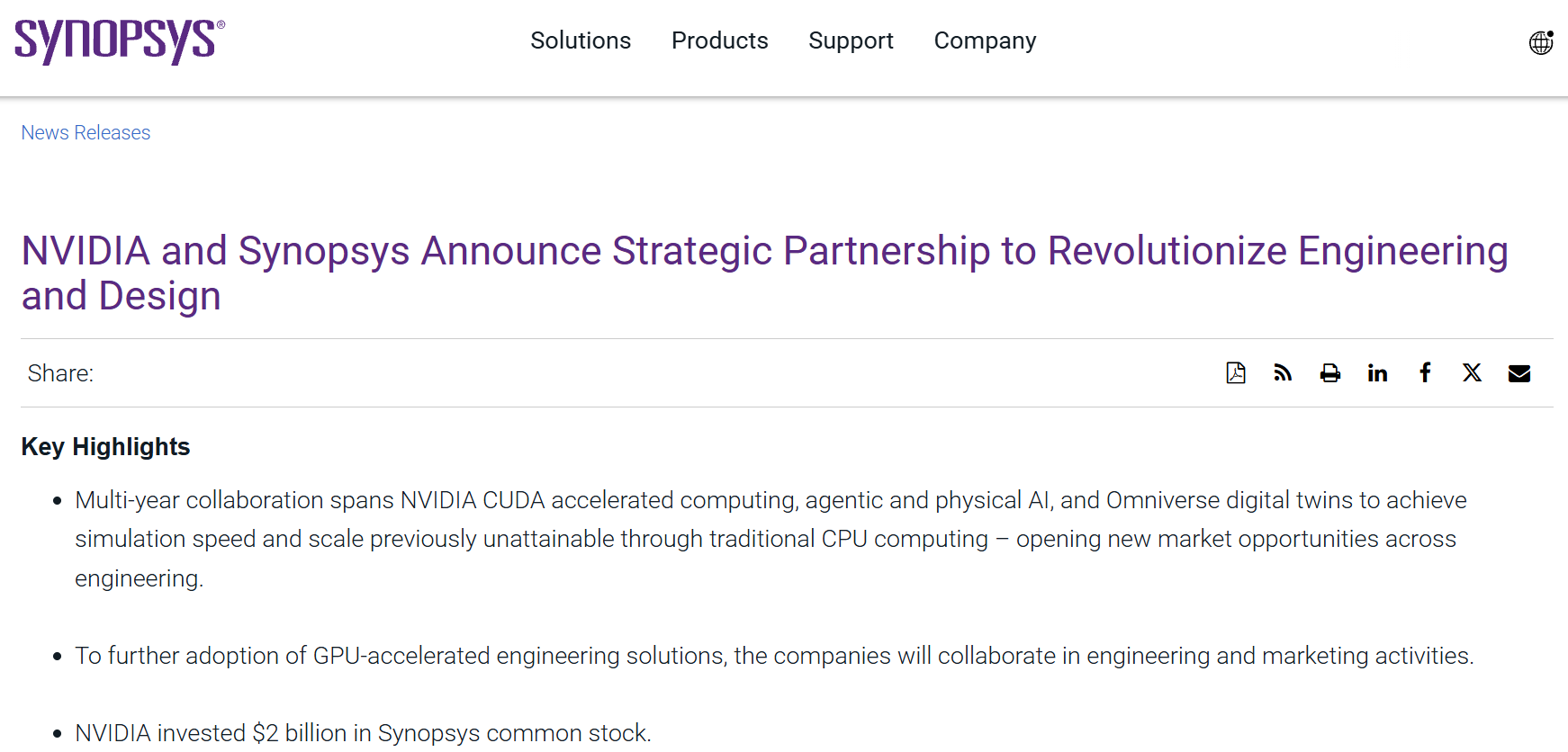

On December 1, 2025, NVIDIA announced an approximately $2 billion equity investment in Synopsys, one of the world’s leading EDA (Electronic Design Automation) companies.

TL;DR:

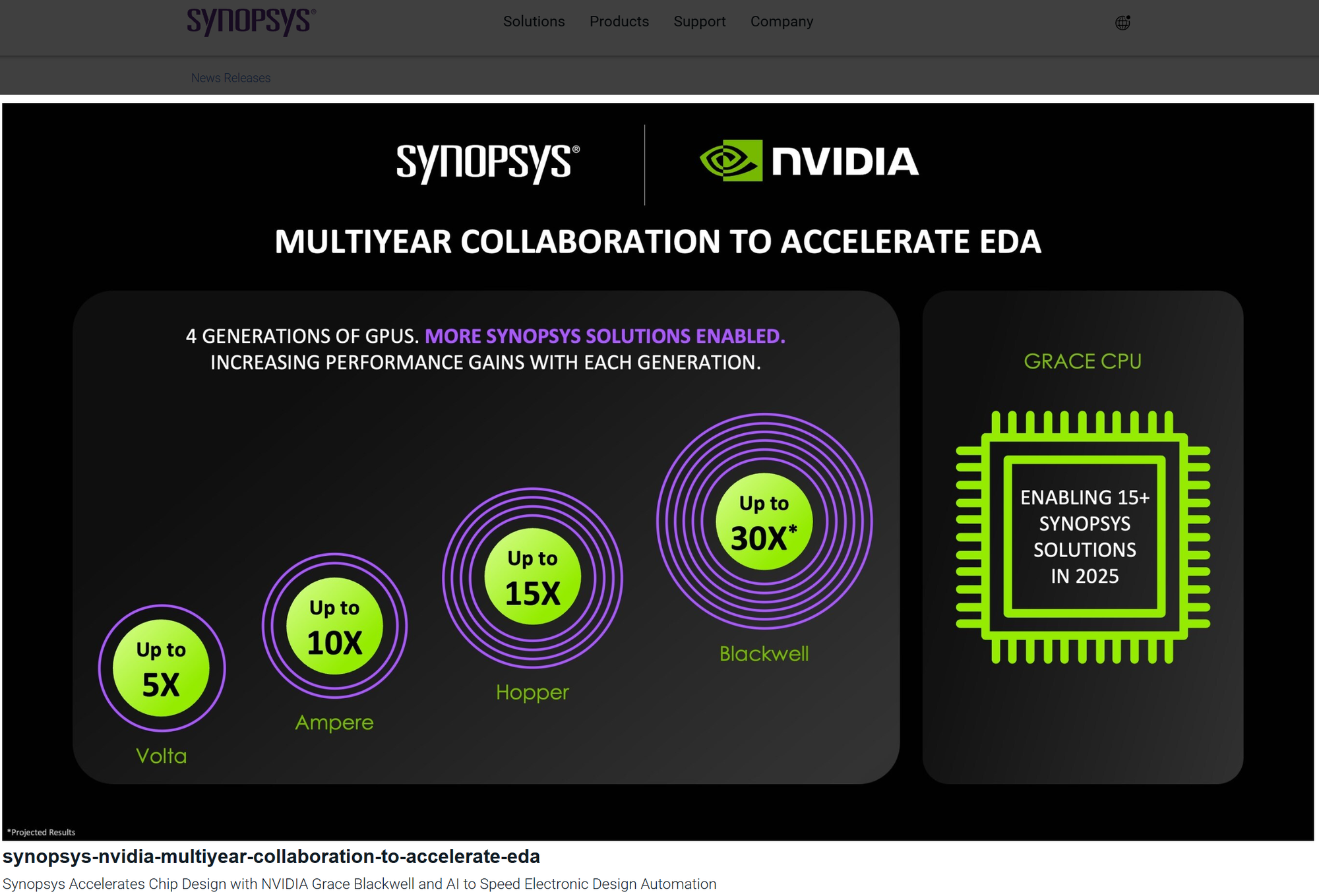

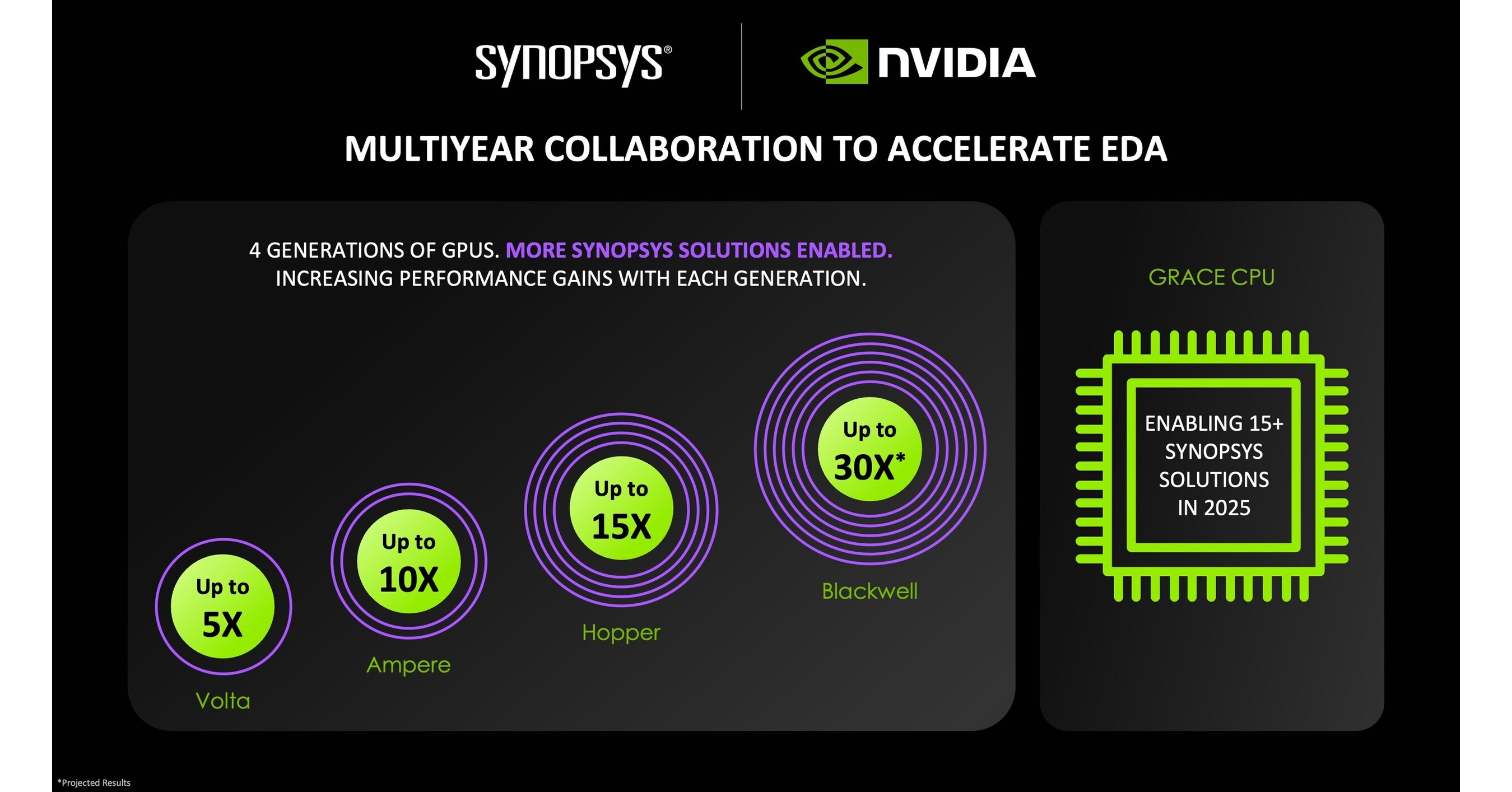

The collaboration between Synopsys and NVIDIA aims to tightly integrate NVIDIA’s CUDA GPU-accelerated computing with Synopsys’ EDA and engineering-simulation technologies, enabling ultra-high-speed design and simulation workflows that were previously impossible with CPU-based architectures.

You will miss the essence if you interpret NVIDIA’s “strategic investment” in Synopsys as a simple financial transaction. The correct frame is not “equity ownership” but rather the redefinition of workflows, compute layers, and data boundaries across the semiconductor ecosystem.

EDA, foundry, and AI are being reconfigured into a single integrated stack.

Before diving deeper, let us establish the verifiable facts.

According to press releases from both Synopsys and NVIDIA, NVIDIA executed an investment of roughly $2B, corresponding to a reported $414.79 per share.

If one divides those figures, the transaction corresponds to approximately:

≈ 5,000,000 shares = $2,000,000,000 / $414.79

This “share count” is an arithmetic back-calculation based solely on reported investment amount and share price. It is not an officially disclosed figure.

Another key axis is the substance of the collaboration.

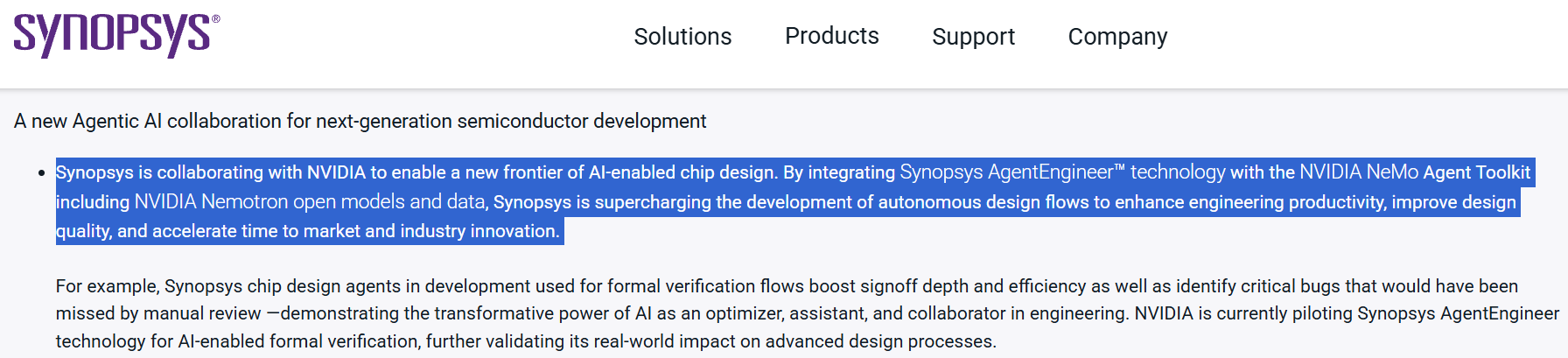

At GTC 2025, NVIDIA and Synopsys publicly discussed multiple joint initiatives, including AI-agent-based IC design assistance (reported under the name “AgentEngineer”).

In other words, this is not a “sudden relationship,” but a natural extension of a long-term direction to reinvent EDA productivity using Agentic AI, culminating in this capital and business integration.

Why NVIDIA Invested in Synopsys

In the AI era, the bottleneck is no longer only in model training.

Better models require better chips, and better chips require more design-space exploration, more verification, and more physical-closure iterations—all handled by EDA.

There is one critical shift:

Past:

EDA = “software for automating chip design”

Now:

EDA = “industrial AI and compute consumer that solves massive optimization problems + an operating system containing design and manufacturing knowledge”

Chip design has always been an optimization problem, but constraints keep increasing.

At 2nm/3nm nodes, PPA (Performance/Power/Area) optimization interweaves process, packaging, architecture, power, thermal behavior, and reliability.

As 3D-IC, chiplets, HBM, and advanced packaging (CoWoS, interposers, etc.) grow, closure is no longer per-chip but system-level.

Thus, EDA is no longer a “tool”—it becomes a productivity platform.

Why GPUs matter

GPUs excel at the types of mathematical operations widely used inside EDA.

For example: SPICE circuit simulation involves heavy matrix computation. Placement in digital P&R is fundamentally a large matrix-optimization problem.

Recently, the volume of AI-driven EDA research has exploded (MLCAD, DAC, ICCAD, DATE, ASPDAC, VLSI-DAT, etc.).

As semiconductor designs grow more complex and engineering talent becomes scarce, AI agents and automated exploration have become essential.

Many segments of EDA can benefit from GPUs—although many bottlenecks remain NP-hard and CPU-centric tasks still exist.

Still, industry consensus expects GPU demand inside EDA workflows to surge.

NVIDIA’s Perspective on Synopsys

NVIDIA does not view this as “expanding GPU sales.”

Synopsys represents the deepest industrial workflow where NVIDIA can embed GPUs as the standard compute layer.

To build the best AI models, you need the best chips.

To build the best chips, you need state-of-the-art EDA.

State-of-the-art EDA is rapidly becoming GPU-accelerated.

Once GPU vendors and EDA vendors join forces, GPU-native EDA spreads across industry.

Any company using GPU-native EDA becomes dependent on GPU clusters to achieve competitive turnaround times.

At this point, NVIDIA’s primary interest in Synopsys lies in:

- The compute consumed across the entire EDA workflow

- The vast design and verification data generated by EDA

- The distribution channels that connect EDA to foundries, packaging houses, and system OEMs

And that is not all.

With the acquisition of Ansys, Synopsys has become a full-scale multiphysics simulation company, spanning fluid dynamics, mechanical physics, optical and electromagnetic simulation.

This accelerates NVIDIA’s broader strategy around Digital Twins, AI Factories, and AI Foundries.

EDA tools are notoriously sticky due to sensitive IP and workflow inertia.

Once installed, they are rarely replaced because doing so requires changing entire design flows and retraining engineering teams.

NVIDIA gains long-term platform entrenchment by embedding itself into these workflows.

Synopsys’ Perspective on NVIDIA

This investment represents a strategic alliance to redefine product development in the AI era.

Agentic AI becomes a real product—not just a demo—only when three pillars exist simultaneously:

- Massive compute infrastructure

- Domain knowledge (EDA algorithms, circuit-design expertise)

- Data and distribution channels (Synopsys' internal design data + foundry relationships)

Synopsys’ strengths:

domain knowledge, proprietary data, distribution channels

NVIDIA’s strengths:

compute, AI stack

The vision behind AgentEngineer—“AI agents that design chips”—cannot be commercialized without the combined strengths of both companies.

EDA in the AI Era: The Path an Agent Must Walk

To generate real economic value in EDA, AI agents must replace essential loops in product development, not merely generate text.

What matters to designers:

- Finding better solutions faster (optimization)

- Detecting failures precisely and early (verification)

- Reducing iteration count (convergence)

Traditionally, this loop has relied on human expertise.

Agentic AI introduces an automated decision-maker into the flow.

But EDA is not a single tool—it's a chain of dozens of tools customized to organizational, foundry, IP, process, and packaging constraints.

Thus, inserting an agent requires an operating model that spans the entire toolchain, not just individual tools.

The operating model ultimately comprises:

- logs, execution traces, quality metrics (data)

- large-scale parallel exploration (compute)

- safety mechanisms (verification and accountability)

When NVIDIA partners strategically with Synopsys, it gains the ability to normalize the path agents walk—on top of the NVIDIA compute and software stack.

This is more than “GPU acceleration.”

EDA’s iterative workloads become native workloads of the NVIDIA platform.

From that point on, industry competition shifts from:

“Who has the better tool?” → “Whose workflows are standardized, agent-driven, and integrated into the compute-data-distribution stack?”

The Future of EDA

The EDA of the future will not revolve around UI commands or manual scripting.

Instead, engineers will provide goals and constraints, and AI agents will:

- generate design alternatives,

- run extensive tests,

- narrow down candidates,

- learn from failures, and

- autonomously plan subsequent experiments.

In this paradigm, the core asset is workflow data, not code.

Examples of such critical data include:

- which decisions led to convergence under which constraints,

- which decisions caused Power/Performance/Area regressions,

- how these behaviors repeat across different processes/libraries/packaging conditions.

Because this data is deeply entangled with customer IP, it is extremely difficult to collect externally.

Thus, the “EDA vendor + customer relationship” becomes a powerful competitive barrier.

What NVIDIA wants in this space

NVIDIA does not intend to rebuild the entire EDA stack from scratch.

Rather, it aims to control the computational substrate consumed by the agentic operating system.

GPUs are not only ideal for AI training but also for large-scale exploration and simulation.

When the long-standing belief that “EDA belongs to CPUs” breaks, the industry’s performance–cost frontier shifts.

Control over that frontier becomes the new basis of competitive power.

Foundry Industry: Toward an Integrated Design–Manufacturing Platform

The foundry’s strategic asset has always been PDK/DTCO.

Even if AI agents perform design tasks, the real world is ultimately governed by process constraints.

Thus, foundries will evolve into “design platforms” on which AI agents operate.

- PDKs will no longer be passive rule sets but constraint interfaces that AI agents read and interpret.

- Signoff will shift from a post-verification step to a real-time constraint enforcer during design exploration.

This means:

- foundries will become more tightly coupled with tools,

- tools will become more tightly coupled with AI agents,

- and dominance will hinge on who defines the standards first across this triangle.

Cloud Industry: Security and Governance

Fabless companies and foundries traditionally prefer on-premise compute due to IP sensitivity.

Most maintain their own compute farms and install EDA tools locally.

But GPU-native EDA requires heavy GPU resources.

Currently, GPUs are difficult to procure and prohibitively expensive for many companies.

The NVIDIA–Synopsys alliance is powerful here:

- NVIDIA controls the AI infrastructure (GPUs, cloud, software stack, security).

- Synopsys knows customer IP-governance requirements better than anyone.

Together, they can define the “standard architecture for secure AI-EDA execution.”

EDA Licensing Model Is Shifting From ‘Feature-Based’ to ‘Token-Based’

Today, EDA licenses are typically feature-based.

For example: certain process nodes require specific features, and customers purchase a fixed number of licenses for those features.

With Agentic AI, customers no longer want “features”; they want tokens.

Pricing will increasingly reflect:

- agent usage (inference tokens / task counts)

- computational load (GPU-hours / cluster usage)

- performance outcomes (reduced iterations, TAT improvements)

This model is attractive to both NVIDIA and Synopsys because it transforms EDA economics into GPU-hour consumption economics.

Competitive Dynamics: From “EDA vs. EDA” to “Alliance vs. Alliance”

The competitive battlefield is no longer tool-to-tool.

It is now a three-axis alignment problem:

- EDA domain expertise

- Foundry and packaging constraints

- AI compute infrastructure (stack + operations)

NVIDIA–Synopsys represents the combination of EDA + compute infrastructure.

This forces every other player—EDA vendors, cloud providers, foundries—to choose an alliance.

The next decade will be dominated by partnerships and standard-setting battles.

What Synopsys Gains

Synopsys stands to benefit in three major ways:

1. A new narrative focused not on “speed” but on “convergence.”

GPU acceleration matters only when it enables more exploration with lower total TAT, not merely a few percent runtime improvement.

If AI agents can run many experiments cost-effectively, design teams will fundamentally change how they operate.

2. Access to the operational stack needed to commercialize Agentic AI.

AI agents require more than models—they need monitoring, safety guards, rollback systems, audit trails, and customer-specific policies.

Coupling with NVIDIA’s AI Enterprise stack accelerates industrialization of agent-based EDA.

3. Trust and channel advantages.

NVIDIA is the symbolic platform company of the AI era.

When Synopsys presents agentic EDA jointly with NVIDIA, customer organizations—spanning engineering, foundry teams, IT, security, and executive management—are more likely to view it as a direction, not an experiment.

This shortens internal approval cycles and increases adoption.

What NVIDIA Gains

NVIDIA also gains three clear advantages:

1. TAM Expansion

EDA already consumes HPC; AI-agent-driven exploration will multiply simulation and optimization workloads.

EDA becomes a massive workload independent of AI training cycles, allowing NVIDIA to deepen its position as the indispensable compute layer for semiconductor R&D.

2. Platform Lock-In

Lock-in in EDA workflows is fundamentally different from that in gaming engines or 3D tools.

EDA flows—once validated—are rarely changed because the risk and cost are enormous.

If NVIDIA becomes the “default acceleration layer” for EDA, lock-in lasts a decade or more.

3. Influence in Standard-Setting

AI agents need standard interfaces:

- log formats

- constraint languages

- experiment definitions

- quality metrics

- connections to foundry and packaging rules

Joint research with Synopsys positions NVIDIA to influence these standards at their inception.

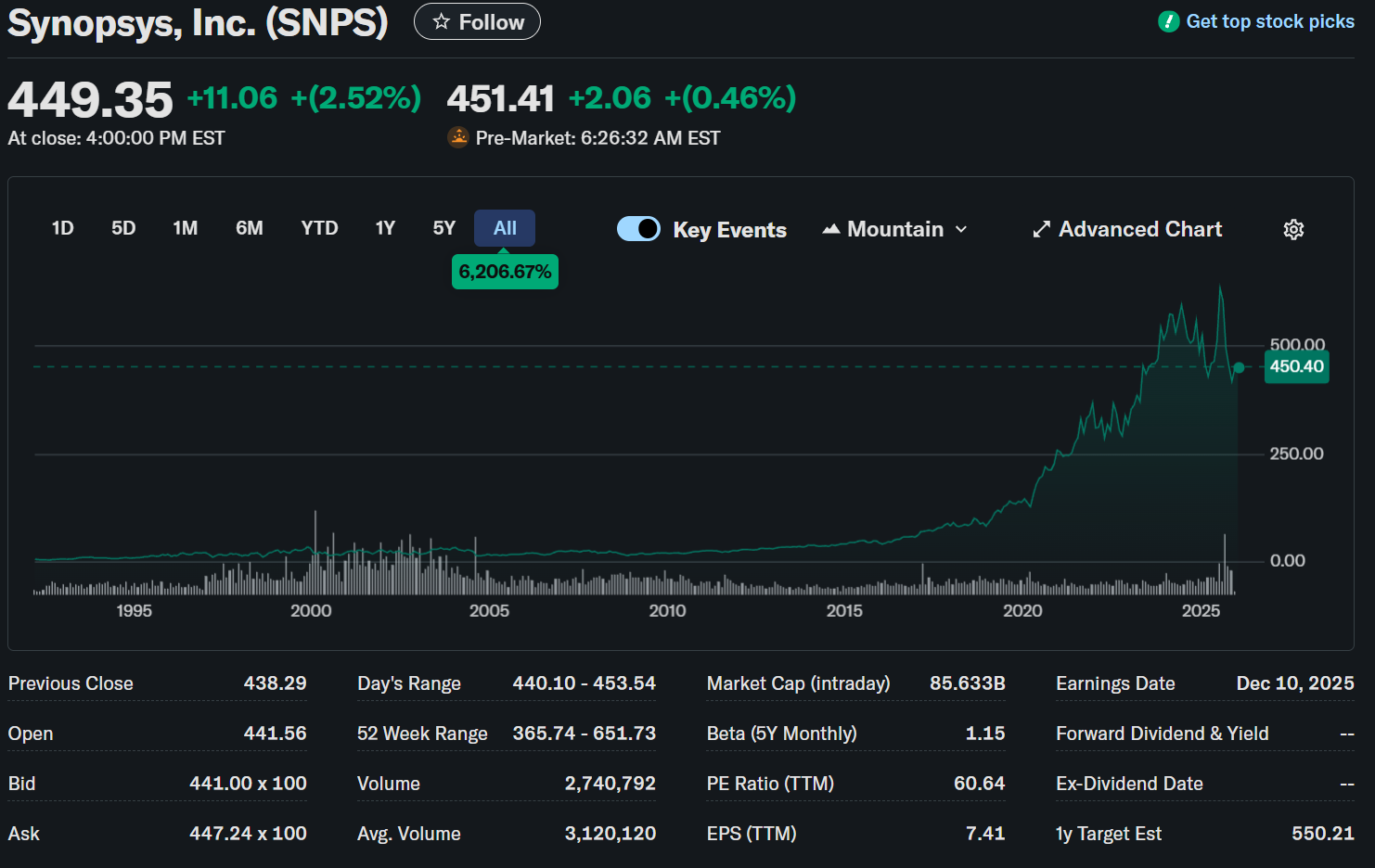

Impact on Stock

On the announcement date, Synopsys shares jumped 8%, and NVIDIA’s stock rose 2%, reflecting strong market approval.

Industry analysts noted that the deal demonstrates how NVIDIA’s AI ecosystem is expanding into chip design tools and system engineering.

Observers also noted NVIDIA’s growing pattern of deploying capital to major customers to accelerate GPU adoption.

For example:

- Up to $100B investment + cloud provisioning for OpenAI

- Up to $15B (with Microsoft) invested in Anthropic

In this context, expanding into EDA via Synopsys is seen as part of NVIDIA’s strategy to pull the entire chip-design and chip-manufacturing ecosystem onto its platform.

CEO Messages: Meaning of the Partnership

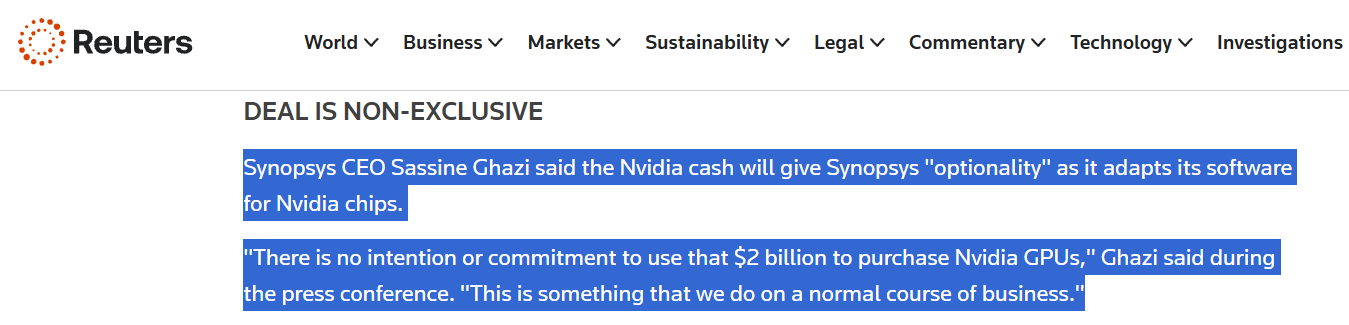

Both CEOs—Sassine Ghazi (Synopsys) and Jensen Huang (NVIDIA)—emphasized that this is not an exclusive partnership.

Synopsys remains open to working with other semiconductor companies, and the investment does not bind Synopsys to purchase NVIDIA GPUs.

Thus, Synopsys maintains independence, and the partnership is explicitly non-exclusive.

Jensen Huang, NVIDIA CEO

He stated that CUDA GPU-accelerated computing is reinventing design, enabling simulations from the atomic level to full systems at unprecedented speed and scale, creating “a complete digital twin inside the computer.”

He emphasized that NVIDIA will empower engineers to invent extraordinary products of the future.

Sassine Ghazi, Synopsys CEO

He noted that next-generation intelligent systems require deeply integrated engineering across electronics and physics, accelerated by AI computing.

He asserted that no combination other than NVIDIA + Synopsys can deliver such an AI-driven holistic design platform.

Both CEOs underscored that the partnership is intended to fundamentally improve design productivity, precision, and cost structures through AI-accelerated EDA.

Press Release Highlights from NVIDIA & Synopsys

Broad EDA Acceleration

The two companies announced plans to significantly accelerate a wide range of high-compute engineering applications using NVIDIA’s CUDA-X libraries and AI-Physics technologies, including:

- chip design,

- physical verification,

- molecular simulation,

- electromagnetic analysis,

- optical simulation.

Simulations that once required weeks on CPU-based systems can now be completed within hours on GPUs, enabling entirely new design and verification workflows across industries such as aerospace, automotive, energy, and healthcare—not just semiconductors.

Autonomous Design via Agentic AI

Synopsys will integrate its Agent technologies with NVIDIA’s Agentic AI stack, including:

- NIM microservices,

- NeMo toolkits,

- Nemotron models.

This integration enables AI agents to participate autonomously in EDA and simulation workflows.

This goes beyond reinforcement-learning-based optimization; the long-term vision is that engineers specify targets, and AI agents autonomously explore and execute the design process.

Digital Twins

Using NVIDIA Omniverse and Synopsys Cosmos, the companies will create high-fidelity digital twins across:

- semiconductors,

- robotics,

- aerospace,

- automotive,

- energy,

- healthcare.

These digital twins allow complete design, testing, and validation in virtual environments, reducing development cycles and mitigating physical prototyping risks.

Cloud Delivery & Joint Go-to-Market

The companies also plan to offer GPU-accelerated engineering solutions via the cloud so that even small and midsize design teams can access high-performance computing.

Synopsys already resells and supports NVIDIA Omniverse technology through its global distribution channels, and this partnership will deepen that GTM alignment.

Summary of Strategic Intent

NVIDIA aims to reshape the traditionally CPU-dominated EDA ecosystem into a GPU-driven design and simulation paradigm, thereby expanding the addressable market for its hardware and AI stack.

Synopsys seeks to accelerate the creation of a next-generation, AI-native EDA platform using NVIDIA’s compute and AI technologies.

Both companies emphasize that the partnership is open, non-exclusive, and aimed at industry-wide transformation—not a closed, vendor-locked system.

Longstanding Technical Cooperation Before the Investment

NVIDIA and Synopsys have collaborated for years, even before this investment.

GPU Acceleration in PrimeSim (Circuit Simulation)

At GTC 2023, Synopsys reported up to 30× speed-ups in its PrimeSim circuit simulator using NVIDIA GPUs.

(SPICE equation solving is fundamentally a matrix problem, which maps well to GPU parallelism.)

GPU Acceleration in Proteus (Optical Lithography)

Synopsys also achieved nearly 20× acceleration in its Proteus optical lithography simulation platform.

These demonstrated the clear superiority of GPU parallelism in matrix-heavy EDA workloads.

cuLitho: NVIDIA’s Push into Semiconductor Manufacturing Simulation

In March 2023, NVIDIA launched cuLitho, a GPU-accelerated library for computational lithography (OPC and related processes), in collaboration with:

- TSMC

- ASML

- Synopsys

NVIDIA claimed up to 40× acceleration of OPC processing compared to CPU platforms, dramatically reducing photomask preparation times.

Synopsys’ OPC platform Proteus™ was optimized for cuLitho, and major foundries like TSMC adopted it enthusiastically.

The Implications

NVIDIA has been methodically executing a strategy to accelerate:

- chip design (EDA),

- chip manufacturing (computational lithography),

- system-level simulation.

In this broader strategic arc, deeper integration with Synopsys was inevitable.

NVIDIA + Synopsys: Products Already Visible

The two companies are already shipping integrated solutions.

Examples:

- PrimeSim GPU acceleration

- AI-driven design automation features within Synopsys.ai

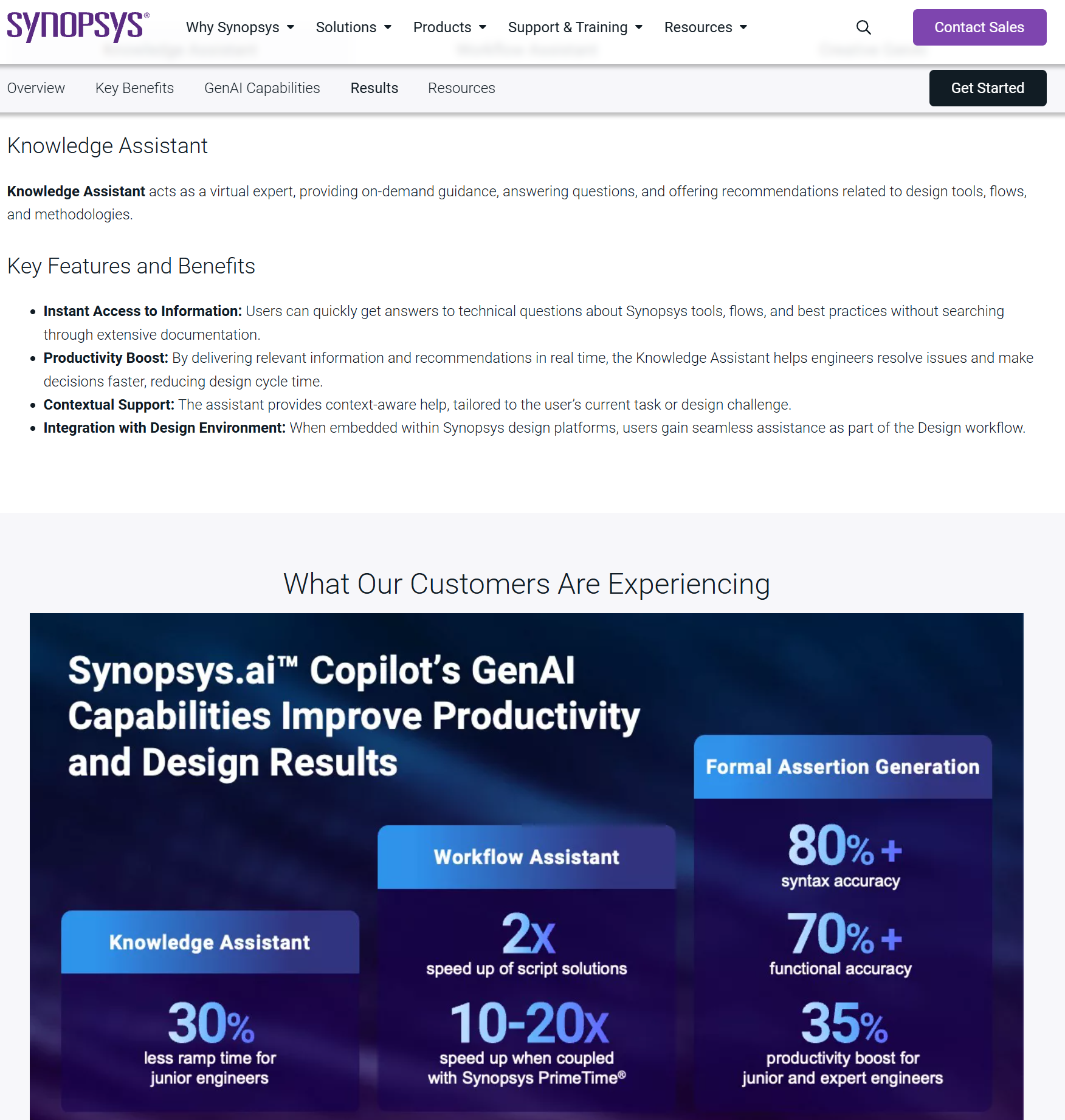

- Knowledge Assistant (KA) built using NVIDIA NeMo and NIM

Synopsys publicly stated that KA uses NVIDIA’s LLM frameworks to enable:

- natural-language queries inside EDA tools,

- log interpretation and troubleshooting,

- design insights derived from proprietary internal datasets.

Thus, NVIDIA’s AI stack is already deeply embedded in Synopsys’ AI EDA vision.

NVIDIA Corporate Strategy: “AI Foundry”

Over the last five years, NVIDIA has redefined itself from a GPU hardware company to a full AI computing platform.

In the 2010s, NVIDIA’s business centered around GPUs for gaming and professional graphics.

Starting in 2016, with the deep learning boom, the company pivoted aggressively into datacenter AI accelerators, achieving exponential growth.

Since 2018, Jensen Huang has described NVIDIA as:

“The company building the steam engine of the AI era.”

NVIDIA now provides not only chips but:

- NVLink/NVSwitch interconnects,

- DGX systems,

- CUDA software stack,

- AI frameworks (cuDNN, TensorRT, etc.),

- DGX Cloud,

- enterprise AI software.

This stack enables end-to-end AI development as a single platform.

The AI Foundry Concept

Jensen Huang likens the AI Foundry of the future to the steel mills and power plants of the industrial age:

“In the AI era, data and compute are the fundamental capital resources.”

An AI Foundry is an NVIDIA-powered “factory” where:

- customers bring ideas,

- NVIDIA provides model-building infrastructure.

NVIDIA AI Foundry includes:

- DGX Cloud (mass-scale GPU clusters),

- NVIDIA AI Enterprise,

- pretrained LLMs and model pipelines,

- tools for fine-tuning, serving, and lifecycle management.

In this vision, EDA sits at the core of the loop:

“AI designing AI chips.”

The future AI Foundry may ultimately support:

- model creation,

- chip creation,

- system creation—

all generated within the same NVIDIA-run infrastructure.

EDA becomes the mechanism that makes chip-level automation possible.

NVIDIA’s Dependency on EDA Vendors

NVIDIA is one of the world’s largest consumers of commercial EDA tools.

For its latest GPUs and SoCs, NVIDIA uses:

- Synopsys digital implementation tools,

- Synopsys timing/power/verification solutions,

- extensive Synopsys interface IP,

- Cadence’s analog/mixed-signal tools and AI engines in some blocks.

Synopsys previously reported DSO.ai being used on NVIDIA GPU designs (Hopper), although detailed PPA results remain confidential.

Cadence’s Cerebrus was also evaluated for Blackwell GPU designs.

NVIDIA has therefore already seen the impact of AI-driven design automation firsthand, which likely reinforced its motivation to invest in Synopsys.

Will NVIDIA Build Its Own EDA Tools?

Industry consensus is:

NVIDIA is unlikely to develop a full EDA suite.

Reasons:

- EDA requires decades of accumulated algorithms, heuristics, and datasets.

NVIDIA lacks access to diverse customer IP needed to train robust design algorithms. - Most big tech companies only build internal tools for specialized steps, not full EDA stacks.

- GPU acceleration is NVIDIA’s strategic sweet spot, not complete toolchain development.

NVIDIA is more likely to:

- build GPU-accelerated libraries (like cuLitho),

- co-develop modules with EDA vendors,

- create agent frameworks for EDA,

- selectively enter niche areas with high synergy.

NVIDIA’s ROI is higher when it influences EDA without owning it.

This arrangement benefits both parties:

- Synopsys maintains independence and trust.

- NVIDIA gains access and deep integration without competing with EDA vendors.

- The EDA ecosystem aligns around NVIDIA GPUs instead of alternatives (AMD, Intel).

Synopsys Strategy and Organizational Transformation

Synopsys has been broadening its scope across:

- EDA,

- semiconductor IP,

- physics simulation,

- system engineering.

In January 2024, Synopsys announced a $35B acquisition of Ansys, completed in July 2025.

This transformed Synopsys into a comprehensive engineering-simulation powerhouse covering:

- semiconductor design,

- multiphysics (thermal, structural, EM, optical),

- automotive and aerospace simulation,

- digital twins.

Synopsys reported its total addressable market (TAM) expanded to $31B, combining:

- ~$18B EDA + IP market

- ~$13B Ansys physics-simulation market

This enables true chip-system co-optimization, essential for:

- AI systems,

- autonomous vehicles,

- aerospace,

- robotics,

- advanced compute systems.

The NVIDIA partnership amplifies this by enabling Omniverse-powered digital twins.

Why Synopsys?

Several structural reasons explain why Synopsys was the ideal partner for NVIDIA.

- Synopsys is the global No.1 EDA company

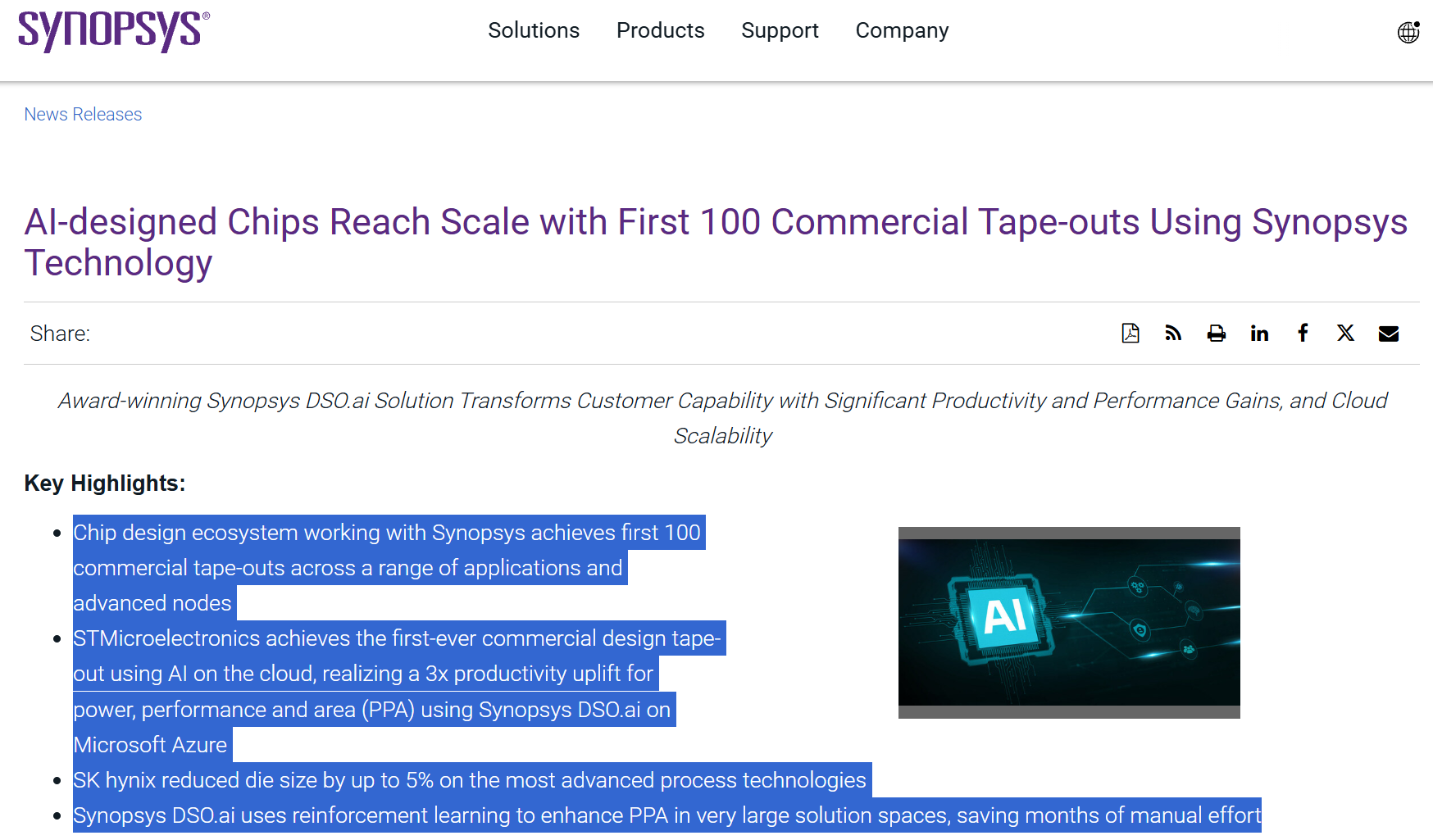

Along with Cadence, Synopsys dominates the EDA market, with leadership particularly strong in digital design automation (implementation, verification, signoff). - Synopsys has led the commercialization of AI-driven EDA

Synopsys introduced the world’s first commercial AI-driven placement & routing tool, DSO.ai, in 2020.By 2023, Synopsys announced:Source:

https://news.synopsys.com/2023-02-07-AI-designed-Chips-Reach-Scale-with-First-100-Commercial-Tape-outs-Using-Synopsys-Technology- 100+ commercial tape-outs utilizing DSO.ai

- Up to 25% PPA improvements

- Up to 3× productivity gains

- Synopsys expanded AI from digital P&R to verification, testing, and full-chip optimizationExample:

On Samsung GAA nodes, AI-driven optimization produced 12% performance gains and 25% power reductions.- VSO.ai for verification

- TSO.ai for test optimization

- Full AI integration within Synopsys.ai suite

- AI flows certified for advanced nodes (3nm & GAA processes)

Because Synopsys has become the default leader in AI EDA, partnering with them allows NVIDIA to:

- expand GPU adoption across the entire semiconductor value chain,

- embed CUDA/GPU acceleration deep into engineering workflows,

- influence future standards for AI-driven design.

This partnership embodies the shared objective of shifting from:

CPU-centric → GPU-accelerated, AI-orchestrated chip design.

AI-Based EDA Competition: Technical Comparison & Adoption Speed

The competition in AI EDA is largely between Synopsys (DSO.ai) and Cadence (Cerebrus), with Siemens beginning to follow through Extreme EDA Suite.

Key Differences Between DSO.ai and Cerebrus

| Category | Synopsys DSO.ai | Cadence Cerebrus |

|---|---|---|

| Core Approach | Reinforcement Learning | Reinforcement Learning + JedAI analytics |

| Focus Area | Digital P&R first, then extended | Broader (analog, PCB/package, mixed-signal) |

| Market Traction | Highest commercial success | Strong, especially in analog/mixed-signal |

| Unique Strength | Proven PPA gains across many customers & nodes | Deep integration with Cadence Virtuoso ecosystem |

Both pursue RL-based design-space exploration, but Cadence emphasizes the use of its JedAI platform to analyze large design datasets for intelligent feedback loops.

Synopsys’ strategy was to prove digital success first (P&R), then expand.

Cadence’s strategy is to apply AI more broadly across:

- Analog ICs (Virtuoso)

- PCB/Package design (Allegro)

- Mixed-signal design

Real-World Adoption Cases

AI EDA is most aggressively adopted by teams facing extreme design complexity:

- hyperscalers (Microsoft, Google, Amazon)

- GPU/TPU design teams

- mobile SoC vendors

- AI accelerator startups

Examples:

- Microsoft used DSO.ai for 5nm processor power optimization and achieved 3% total power reduction.

- Cadence Cerebrus reported:

- 8× engineering productivity improvement for 5nm GPU

- 30% leakage reduction for a 4nm server GPU design

Such measurable PPA/TAT improvements create a powerful feedback loop that accelerates AI EDA adoption.

Global Market Insight

The EDA industry shows robust, sustained growth driven by increasing design complexity and AI integration.

Forecasted Market Size

The global EDA market is projected to exceed $24B by 2030, with ~10% CAGR. Source: “Electronic Design Automation Market (EDA) Size & Share Analysis (2025–2032)”

Historically, EDA’s customer base consisted of:

- fabless companies

- IDMs

- foundries

But the AI era has expanded the user base to:

- IT big tech (Google, Amazon, Meta) designing custom silicon

- automotive OEMs

- IoT system providers

- hyperscaler ASIC teams

- AI hardware startups

Bloomberg Intelligence projects AI will increase EDA market CAGR by +2 percentage points, reaching:

11.8% CAGR (2024–2030)

This is nearly double the semiconductor industry’s expected growth (~6%).

EDA, historically 3–4% of chip value, will take a larger portion of the semiconductor value chain.

AI-Driven EDA Ecosystem

AI is fundamentally reshaping how engineers interact with design tools.

Historically, the chip design flow—from specification → RTL → synthesis → P&R → verification → signoff → test—relied on engineers manually iterating through each phase.

With AI, major segments become automatable, especially:

- design-space exploration

- placement optimization

- routing decision-making

- testbench generation

- verification coverage improvement

- automatic test pattern generation

Different AI technologies play unique roles:

Reinforcement Learning (RL)

Used heavily in exploration and optimization tasks.

Graph Neural Networks (GNNs)

Capture structural characteristics of circuits to predict performance trends or viability of placement decisions.

Large Language Models (LLMs)

Transform natural-language specifications and logs into actionable engineering insights:

- interpret EDA logs,

- summarize errors,

- auto-generate SystemVerilog/Verilog code,

- extract formal properties from English specifications,

- assist with debugging and documentation.

The Strategic Reality

EDA is becoming a human–AI co-design environment, where engineers supervise AI agents that automate increasingly large portions of the workflow.

Strategic Directions for EDA Companies in the AI Era

Based on the above analysis, EDA companies must adopt several strategic imperatives:

1. Internalize AI Capabilities & Build Open Ecosystems

- Hire significantly more AI scientists and MLOps engineers

- Integrate external AI technologies (LLMs, RL frameworks, GNN libraries)

- Collaborate with platform providers like NVIDIA to co-develop solutions

2. Evolve into Platform Providers

EDA must shift from tool sales to EDA-as-a-Service:

- cloud-native tools

- usage-based/token-based billing

- customer success partnerships (“co-designer” model)

- broader value-chain involvement from RTL guidance to system-level optimization

3. Provide Integrated, Multi-Domain Solutions

Future products depend on system co-optimization, not isolated chip design.

EDA vendors must integrate:

- chip + package + board + software + physics

- thermal / mechanical / EM simulations

- digital twin technologies

Synopsys/Ansys integration and Cadence’s systems strategy reflect this trend.

4. Prioritize Data Governance & Security

AI EDA requires data:

- anonymized datasets

- synthetic-data generation

- secure AI inference pipelines

- encrypted federated learning

- IP-protection mechanisms preventing reverse engineering from AI outputs

5. Transform Talent & Culture

EDA companies must blend:

- traditional EDA algorithm expertise

- modern AI research culture

- tolerance for rapid iteration and experimentation

- bottom-up innovation from young engineers and customers

Industry leaders like Aart de Geus and Lip-Bu Tan emphasize this cultural shift.

6. Prepare for Geopolitical Fragmentation

EDA companies must:

- navigate export controls

- maintain compliance across US–China technology boundaries

- consider JV or regional partnerships if global block formation increases

- secure core IP while ensuring global adaptability

Conclusion

NVIDIA’s strategic investment in Synopsys represents a defining moment for the EDA industry in the AI era.

EDA companies must treat AI not as a threat but as a catalyst for:

- technological reinvention,

- business model transformation,

- ecosystem-led innovation.

Over the next decade, EDA will become increasingly central to the semiconductor value chain, forming symbiotic partnerships with AI platform companies like NVIDIA.

“AI will reshape EDA, and EDA will accelerate AI.”

The companies that best harmonize this cycle will lead the next generation of semiconductor innovation.