A practicing semiconductor engineer's daily read on global silicon news:

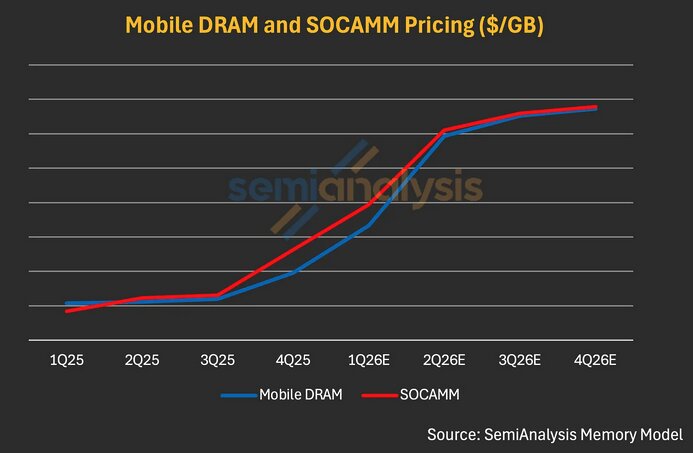

The signals from the first week of May add up to one line: the memory supercycle just got extended by another year. SemiAnalysis sees NVIDIA SOCAMM pricing reaching $13/GB by year-end while TSMC defers High-NA EUV to A13 (2029), pushing 45% of ASML's 1Q26 revenue onto Korean memory — and Qualcomm, MediaTek, and Samsung Foundry all formalized data-center ASIC and silicon-photonics entries the same week, building a second compute/interconnect axis outside NVIDIA-TSMC.

Chase's Take — From a backend engineer's seat, the heaviest line this week is 'no High-NA.' TSMC riding Low-NA + multi-patterning all the way to A13 means mask costs and EPE (edge-placement error) margins blow back up, and OPC/RET libraries plus hotspot fixers get another full cycle. Conversely, SK hynix and Intel taking High-NA first at 14A/HBM in 2027 means memory and server absorb the ramp risk — the inverse of the old setup where mobile SoC carried it. If SOCAMM $13/GB lands, SoC interconnect traffic models need to weight memory payload heavier again, and ASIC design-house diversification (MediaTek, Qualcomm joining) puts downward pressure on IP/EDA license ASPs. Watch-points: ① whether NVIDIA drops SOCAMM2/Vera Rubin pricing guidance at GTC Taipei in June, ② Tower Semiconductor's SiPh revenue guidance on the May 13 1Q26 call, ③ first production wafer-out from SK hynix M15X phase-1 cleanroom (going live this month). Last point — with 43% of KOSPI market cap concentrated in two memory names, Korea is now structurally forcing memory exposure onto global passive flows. When you build the hedge, this is no longer a 'Korea discount' — it's a 'memory beta.'

1. Behind TSMC's High-NA EUV Deferral — Low-NA Through A13 (2029), ASML 1Q26 Korea Revenue 45%

TL;DR — TSMC will defer High-NA EUV (EXE:5200, ~$400m per tool) through the A13 node in 2029 and stay on Low-NA + multi-patterning. The result: 45% of ASML's 1Q26 revenue now comes from Korean memory (SK hynix, Samsung) — a memory-dependent customer mix.

2. AI Demand Strong, Memory Prices Will Go Up — SemiAnalysis: NVIDIA SOCAMM $8 → $13/GB Exit-2026

TL;DR — Brian Wang's NextBigFuture cites SemiAnalysis 'AI Value Capture' — NVIDIA's SOCAMM pricing, locked at ~$8/GB in 1Q26, could break $13/GB by end of 2026. Driver is model revenue scaling (Anthropic run rate $44B → $100B by year-end) feeding back into memory and compute capex.

3. Qualcomm to Supply Custom Chips to a Hyperscaler in December Quarter — Data Center Return Made Official

TL;DR — Per TrendForce: CEO Cristiano Amon used the April 30 earnings call to confirm Qualcomm will ship CPU, inference accelerators, and custom ASICs to one undisclosed hyperscaler starting the December quarter. Built on the Alphawave IP Group acquisition, this brings Qualcomm — which once exited the ARM server business — back into data center.

4. AI Demand to Lift MediaTek Revenue — ASIC Guidance Doubled $1B → $2B, Google TPU Ramping

TL;DR — Per Taipei Times: on the April 30 call, MediaTek CEO Rick Tsai doubled the 4Q26 contribution from the first ASIC project from US$1B to US$2B. The customer was unnamed but is widely identified as Google TPU; second ASIC ramps in late 2027.

5. Samsung Foundry Wins Optical Module Order — Silicon Photonics/CPO Drive Activated, 2H26 Production

TL;DR — Per TrendForce: Samsung confirmed at 1Q26 earnings that it secured a Silicon Photonics order from a major optical-module vendor, with mass production starting 2H 2026. PDK is complete, 300mm wafer platform is ready, and the roadmap extends to a CPO turnkey service in 2029.

6. Relentless Semiconductor Rally — 'Samsung-Hynix' KOSPI Weight 43.1%, Foreigners Returned in April

TL;DR — At the April 30 close, Samsung Electronics + Samsung pref + SK hynix combined market cap reached 43.1% of total KOSPI (KRW 5,407T) — up from 37% at the start of the year, an all-time high for single-industry concentration. Foreigners flipped from a ~KRW 55T 1Q26 net sell to net buys of KRW 1.323T (Samsung), KRW 806.5B (SK hynix), and KRW 300.1B (Samsung pref) in April.