핵심 주장: AI 칩 스타트업의 해자는 TOPS가 아니라 고객이 다음 모델과 다음 실리콘에서도 떠나지 못하게 만드는 시스템 경계에 있다.

제품과 현장 이미지

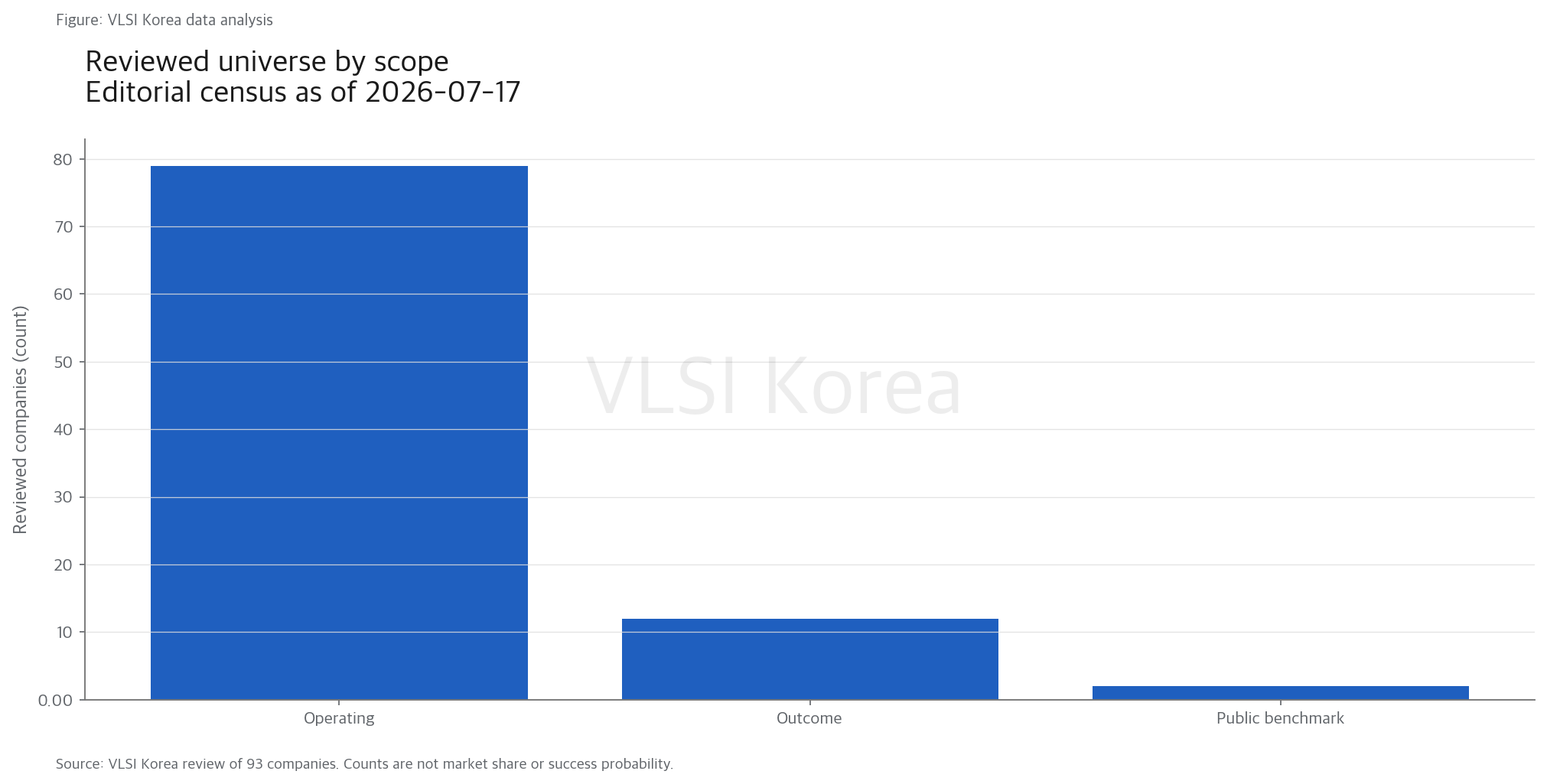

1. 93개를 세되 스타트업·상장사·인수 결과를 섞지 않았다

읽는 법: 회사 수를 늘리는 목적은 이름을 나열하는 것이 아니라 같은 단계가 아닌 회사를 같은 랭킹에 넣지 않기 위해서다.

이 지도는 VC 포트폴리오 목록이 아니다. 칩·chiplet·processor IP·interconnect silicon을 설계하고 공개 silicon 또는 구체 roadmap이 있는 기업을 우선 포함했다. AI software만 파는 회사, 단순 board integrator, 이름 외에 silicon 근거가 없는 stealth 기업은 본표에서 제외하거나 watchlist로 돌렸다.

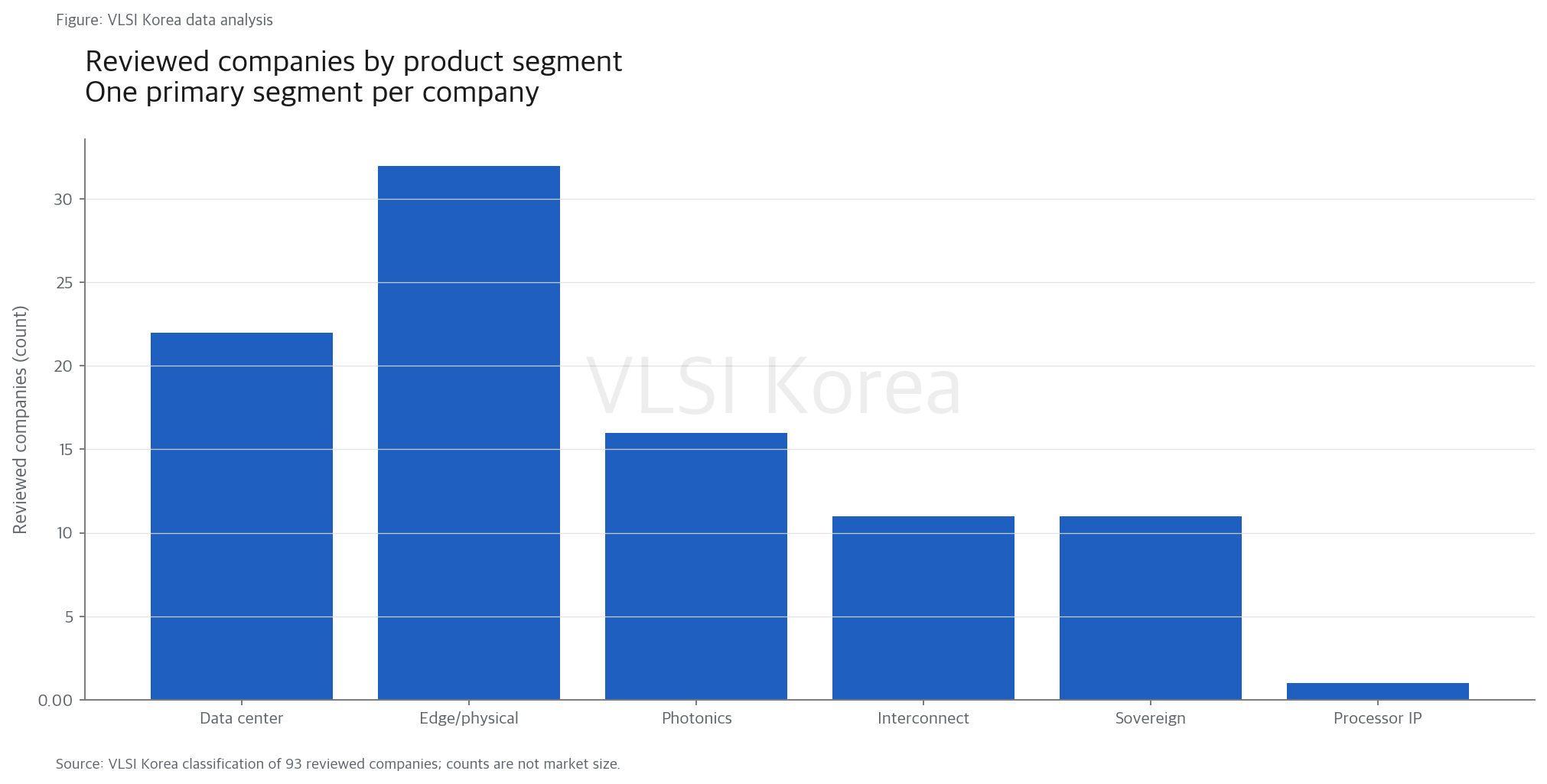

범위는 데이터센터 compute 22곳, edge·physical AI 32곳, photonics 16곳, 전기식 interconnect 11곳, sovereign AI 11곳, processor IP 1곳이다. 한 회사가 여러 시장에 걸쳐도 2026년 주력 제품과 가장 강한 방어선을 기준으로 한 구간만 배정했다.

상장사는 스타트업과 자본구조가 다르지만 감사 매출과 고객 집중도를 공개한다는 이유로 남겼다. Astera Labs와 Ambarella는 public benchmark로 표시했고, Cerebras·Cambricon·중국 GPU 상장사는 실제 운영 기업이므로 A급 증거 표본으로 사용했다.

인수나 영업 종료도 지우지 않았다. Graphcore, Untether AI, Celestial AI, Kinara 같은 결과를 빼면 현재 살아 있는 기업만 보고 성공확률을 과대평가하게 된다. 반대로 인수가 높은 가격에 끝났다고 product-market fit까지 입증됐다고 보지도 않는다.

2. 전체 93개 기업·결과 사례: 증거와 주 해자를 한 줄로 읽기

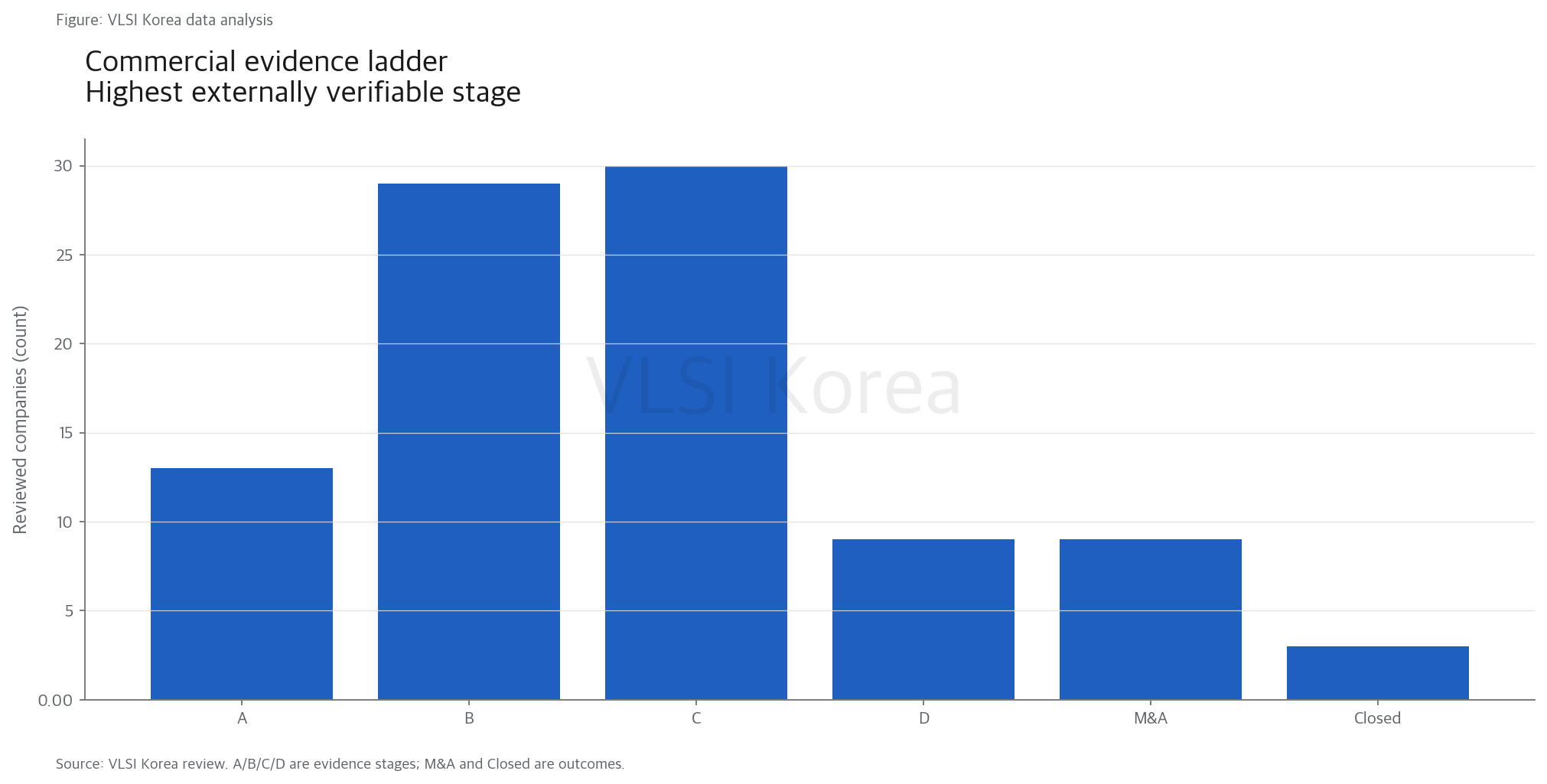

읽는 법: 표의 등급은 누가 더 좋은 칩을 만들었는지가 아니라 공개 자료가 어디까지 왔는지를 뜻한다.

A는 규제·감사 매출과 volume shipment가 확인되는 단계다. B는 named production customer, 판매 가능한 SKU, volume silicon 중 둘 이상을 확인한 단계다. C는 working silicon, sampling, evaluation kit나 design-in은 있지만 반복 매출이 보이지 않는 단계이고, D는 pre-tapeout·simulation·roadmap·unnamed contract 중심이다.

이 규칙은 보수적이다. NDA 아래 실제 매출이 있어도 공개되지 않으면 올려주지 않는다. 동시에 고객 로고가 있어도 paid production인지, 평가인지, cloud instance인지 구분되지 않으면 B의 충분조건으로 쓰지 않는다.

아래 표에서 primary moat는 여섯 관문 중 가장 강한 하나만 기록했다. 실제 회사에는 여러 해자가 겹치지만 하나로 고정해야 분포를 재현할 수 있다. status는 독립 운영, 상장, license, M&A, 종료와 재무위험을 기술점수와 분리한다.

| 기업 | 지역 | 구간 | 증거 | 주 해자 | 2026 상태 |

|---|---|---|---|---|---|

| Cerebras | US | data-center compute | A | architecture asymmetry | public operating company |

| Groq | US | data-center compute | B | architecture asymmetry | independent; non-exclusive NVIDIA license |

| SambaNova | US | data-center compute | B | software switching cost | independent |

| d-Matrix | US | data-center compute | B | memory/interconnect/package | independent |

| Tenstorrent | Canada/US | data-center compute | B | software switching cost | independent |

| Positron | US | data-center compute | B | memory/interconnect/package | independent |

| NextSilicon | Israel/US | data-center compute | B | customer/distribution | independent |

| NeuReality | Israel | data-center compute | B | architecture asymmetry | independent |

| Q.ANT | Germany | data-center compute | B | architecture asymmetry | independent |

| Neuchips | Taiwan | data-center compute | B | architecture asymmetry | independent |

| Etched | US | data-center compute | C | architecture asymmetry | independent |

| Taalas | Canada | data-center compute | C | architecture asymmetry | independent |

| Extropic | US | data-center compute | C | architecture asymmetry | independent |

| Mythic | US | edge/physical AI | C | memory/interconnect/package | independent |

| MatX | US | data-center compute | D | architecture asymmetry | independent |

| Fractile | UK | data-center compute | D | memory/interconnect/package | independent |

| VSORA | France | data-center compute | D | architecture asymmetry | independent |

| Normal Computing | US | data-center compute | D | architecture asymmetry | independent |

| Rivos | US | data-center compute | M&A | capital/supply/sovereignty | acquired by Meta |

| Esperanto Technologies | US | data-center compute | Closed | capital/supply/sovereignty | operations ended; IP acquired |

| Lightmatter | US | photonics | C | memory/interconnect/package | independent |

| Ayar Labs | US | photonics | C | memory/interconnect/package | independent |

| Scintil Photonics | France | photonics | C | memory/interconnect/package | independent |

| Xscape Photonics | US | photonics | C | memory/interconnect/package | independent |

| Avicena | US | photonics | C | memory/interconnect/package | independent |

| DustPhotonics | Israel | photonics | B | memory/interconnect/package | independent |

| Ranovus | Canada | photonics | B | memory/interconnect/package | independent |

| Lightelligence | China/US | photonics | A | customer/distribution | public operating company |

| Salience Labs | UK | photonics | C | architecture asymmetry | independent |

| Lumai | UK | photonics | C | architecture asymmetry | independent |

| Neurophos | US | photonics | D | architecture asymmetry | independent |

| Akhetonics | Germany | photonics | D | architecture asymmetry | independent |

| Oriole Networks | UK | photonics | C | memory/interconnect/package | independent |

| Point2 Technology | US/Korea | interconnect | C | memory/interconnect/package | independent |

| Eliyan | US | interconnect | B | memory/interconnect/package | independent |

| Cornelis Networks | US | interconnect | B | customer/distribution | independent |

| Xsight Labs | Israel | interconnect | B | software switching cost | independent |

| DreamBig Semiconductor | US | interconnect | C | memory/interconnect/package | independent |

| Kandou AI | Switzerland | interconnect | B | memory/interconnect/package | independent |

| Enfabrica | US | interconnect | C | memory/interconnect/package | independent execution uncertain after team/license deal |

| Retym | US | interconnect | D | memory/interconnect/package | independent |

| Celestial AI | US | photonics | M&A | memory/interconnect/package | acquired by Marvell |

| Nubis Communications | US | photonics | M&A | memory/interconnect/package | acquired by Ciena |

| Hyperlume | Canada | photonics | M&A | memory/interconnect/package | acquired by Credo |

| XConn Technologies | US | interconnect | M&A | memory/interconnect/package | acquired by Marvell |

| Alphawave Semi | UK/Canada | interconnect | M&A | software switching cost | acquired by Qualcomm |

| Astera Labs | US | interconnect | A | customer/distribution | public benchmark |

| Rebellions | Korea | sovereign AI | B | capital/supply/sovereignty | independent |

| FuriosaAI | Korea | sovereign AI | B | architecture asymmetry | independent |

| Mobilint | Korea | edge/physical AI | C | edge form-factor | independent |

| DEEPX | Korea | edge/physical AI | B | edge form-factor | independent |

| Cambricon | China | sovereign AI | A | capital/supply/sovereignty | public operating company |

| Moore Threads | China | sovereign AI | A | software switching cost | public operating company |

| MetaX | China | sovereign AI | A | software switching cost | public operating company |

| Biren Technology | China | sovereign AI | A | memory/interconnect/package | public operating company |

| Horizon Robotics | China | edge/physical AI | A | customer/distribution | public operating company |

| Black Sesame Technologies | China | edge/physical AI | A | customer/distribution | public operating company |

| Enflame Technology | China | sovereign AI | A | customer/distribution | public filing-stage company |

| Iluvatar CoreX | China | sovereign AI | A | capital/supply/sovereignty | public filing-stage company |

| Sophgo | China | sovereign AI | B | capital/supply/sovereignty | independent |

| SynSense | Switzerland/China | edge/physical AI | C | edge form-factor | independent |

| Preferred Networks | Japan | edge/physical AI | B | customer/distribution | independent |

| EdgeCortix | Japan | edge/physical AI | B | software switching cost | independent |

| LeapMind | Japan | edge/physical AI | Closed | capital/supply/sovereignty | dissolved; report-level confirmation |

| Axelera AI | Netherlands | edge/physical AI | B | memory/interconnect/package | independent |

| Innatera | Netherlands | edge/physical AI | B | edge form-factor | independent |

| SiPearl | France | sovereign AI | C | capital/supply/sovereignty | independent |

| Semidynamics | Spain | sovereign AI | D | software switching cost | independent IP vendor |

| GreenWaves Technologies | France | edge/physical AI | Closed | capital/supply/sovereignty | operations ended |

| Hailo | Israel | edge/physical AI | B | edge form-factor | independent |

| Inuitive | Israel | edge/physical AI | C | edge form-factor | independent |

| Arbe Robotics | Israel | edge/physical AI | C | customer/distribution | public operating company |

| POLYN Technology | UK/Israel | edge/physical AI | C | edge form-factor | independent |

| SiMa.ai | US | edge/physical AI | B | software switching cost | independent |

| Blaize | US | edge/physical AI | A | customer/distribution | public operating company; going-concern risk |

| Quadric | US | edge/physical AI | B | software switching cost | independent IP vendor |

| Expedera | US | edge/physical AI | B | software switching cost | independent IP vendor |

| Kneron | US/Taiwan | edge/physical AI | C | edge form-factor | independent |

| MemryX | US | edge/physical AI | B | software switching cost | independent |

| BrainChip | Australia/US | edge/physical AI | C | edge form-factor | public operating company |

| Ambient Scientific | US | edge/physical AI | C | edge form-factor | independent |

| EdgeQ | US | edge/physical AI | C | architecture asymmetry | independent |

| Uhnder | US | edge/physical AI | B | edge form-factor | independent |

| Tensordyne | US/Germany | data-center compute | D | architecture asymmetry | independent; renamed from Recogni |

| Kinara | US | edge/physical AI | M&A | customer/distribution | acquired by NXP |

| femtoAI | US | edge/physical AI | C | edge form-factor | independent |

| Graphcore | UK | data-center compute | M&A | software switching cost | acquired by SoftBank |

| Untether AI | Canada | data-center compute | M&A | memory/interconnect/package | transaction with AMD; products ended |

| Efficient Computer | US | edge/physical AI | C | architecture asymmetry | independent |

| EnCharge AI | US | edge/physical AI | C | memory/interconnect/package | independent |

| Rain AI | US | edge/physical AI | C | memory/interconnect/package | independent |

| Akeana | US | processor IP | C | software switching cost | independent IP vendor |

| Ambarella | US | edge/physical AI | A | customer/distribution | public benchmark |

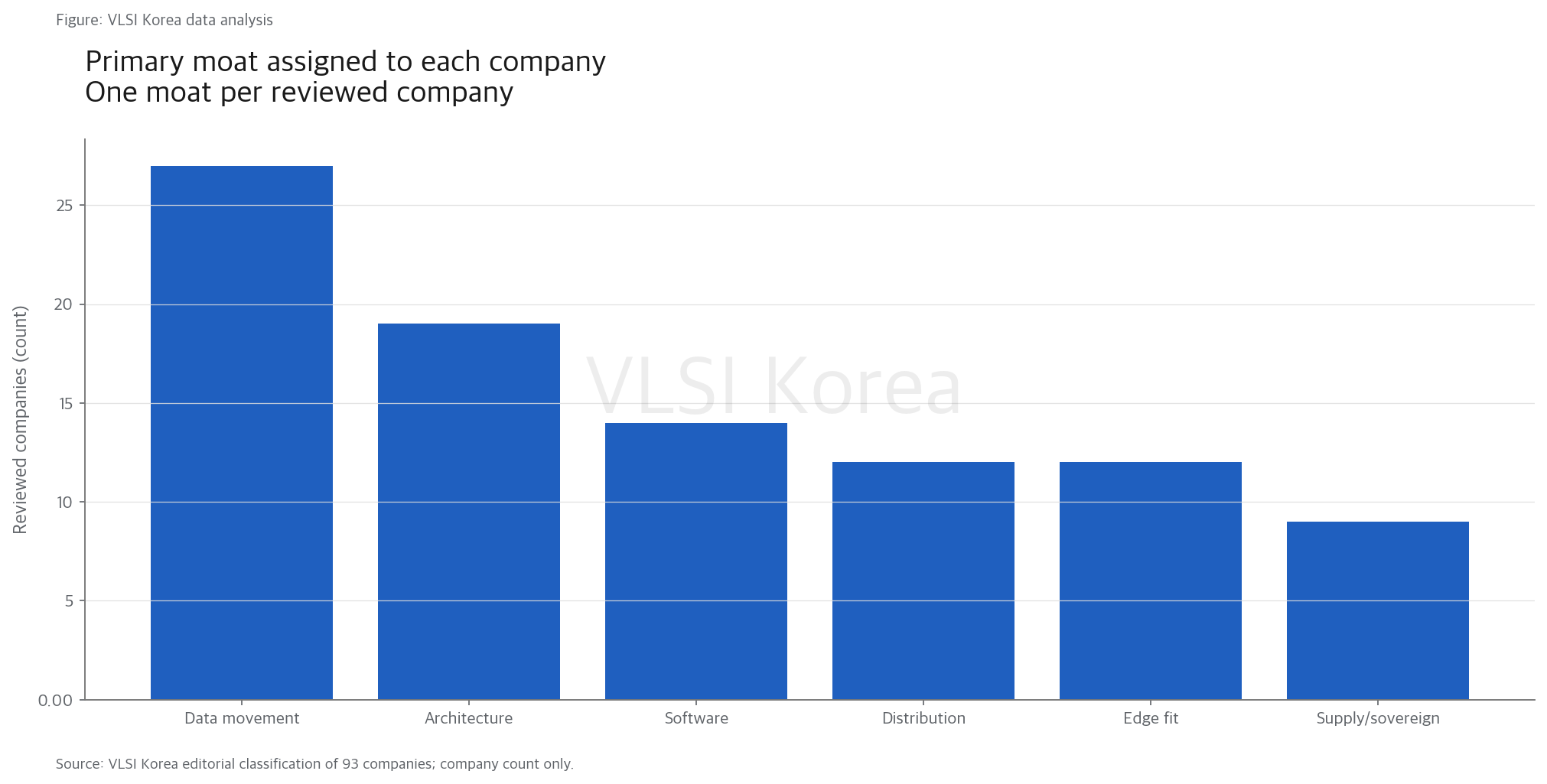

3. 가장 붐비는 해자는 compute가 아니라 data movement다

읽는 법: GPU가 계산을 독점할수록 스타트업은 계산 바깥의 메모리, chiplet, 광 링크와 edge form factor에서 틈을 찾는다.

Lightmatter, Ayar Labs, Celestial AI, Avicena, Eliyan, XConn처럼 연산 자체보다 경계를 파는 기업이 27곳이다. 이들은 HBM 이동, die-to-die PHY, scale-up fabric, optical engine과 package integration을 줄이거나 바꾸려 한다. 복제 난도는 소자 하나가 아니라 foundry PDK, packaging yield, firmware, interoperability와 field reliability의 조합에서 생긴다.

architecture asymmetry 19곳에는 Cerebras의 wafer-scale, Groq의 deterministic dataflow, Etched·Taalas의 workload specialization, neuromorphic·thermodynamic·photonic compute가 들어간다. 이 해자는 가장 설명하기 쉽지만 model mix가 바뀌거나 GPU가 같은 kernel을 최적화하면 가장 빨리 약해질 수도 있다.

software switching cost 14곳은 compiler, runtime, CUDA migration, model coverage와 developer workflow가 핵심이다. Tenstorrent, SambaNova, Moore Threads, MetaX, Xsight와 IP 회사들이 여기에 속한다. benchmark 한 번보다 새 모델 지원시간과 debug 도구, orchestration, backward compatibility가 더 중요한 이유다.

customer·distribution 12곳, edge form-factor 12곳, supply·sovereign 9곳은 기술 사양표에 잘 드러나지 않는다. 자동차 qualification, 산업 channel, 현지 조달, field application engineer, 장기 공급과 local cloud integration은 incumbent가 더 좋은 SKU를 내도 바로 복제하기 어렵다.

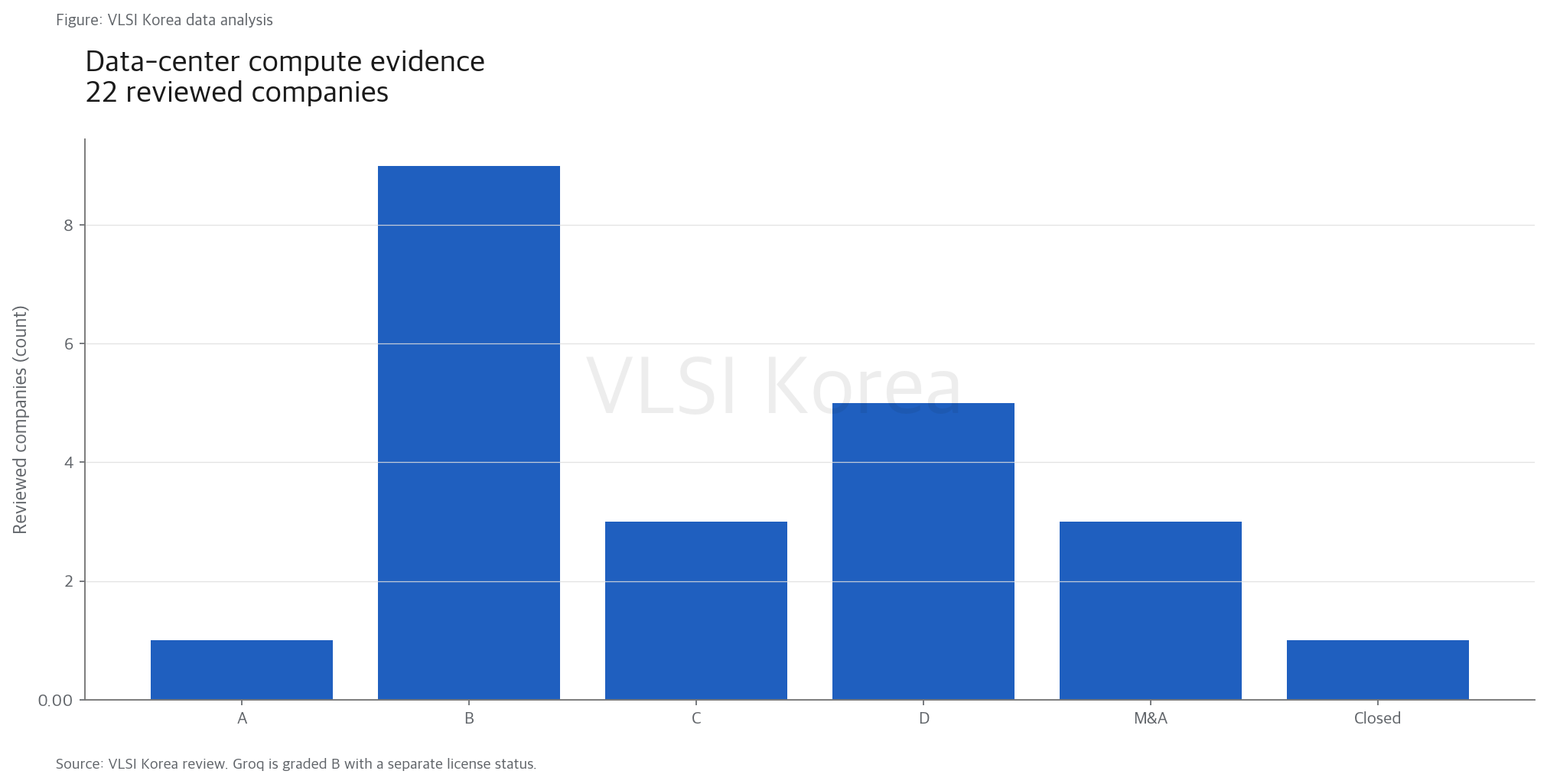

4. 데이터센터 compute: 가장 큰 상방과 가장 좁은 incumbent window

읽는 법: 데이터센터에서 demo chip은 시작점일 뿐이다. 팔리는 단위는 compiler와 support가 붙은 card, appliance, cloud와 rack이다.

Cerebras는 2026년 5월 IPO를 마쳐 규제 공시를 내는 회사가 됐다. wafer-scale architecture가 희귀하다는 사실과 사업 해자가 있다는 주장은 별개지만, 적어도 시스템 출하와 매출, 자본조달을 외부에서 검증할 수 있는 A급 사례가 됐다.

Groq는 흔히 NVIDIA에 인수됐다고 잘못 적힌다. 실제 공식 발표는 비독점 inference technology license이며 창업자와 핵심 인력이 NVIDIA로 이동했지만 Groq는 독립 운영과 GroqCloud 지속을 명시했다. 기술가치 신호와 독립 실행력 약화를 동시에 기록해야 한다.

SambaNova, d-Matrix, Tenstorrent, Positron, NextSilicon, NeuReality, Q.ANT, Neuchips는 B로 묶였지만 해자는 서로 다르다. full-stack dataflow, digital in-memory compute, licensable IP, HBM appliance, institutional acceptance, AI-CPU, photonic processor, recommender specialization을 한 tokens/s 그래프로 비교하면 오히려 정보가 사라진다.

Etched와 Taalas는 specialization의 극단이다. working silicon과 회사 benchmark는 중요한 C급 증거지만, 여러 모델·batch·sequence에서의 독립 검증, rack shipment, compiler 유지비와 반복 주문이 남았다. MatX, Fractile, Normal Computing은 더 큰 주장만큼 D단계 milestone을 먼저 통과해야 한다.

incumbent response window도 짧다. NVIDIA는 GPU뿐 아니라 NVLink, NIC, switch, inference library와 cloud channel을 묶는다. 스타트업이 18-30개월 안에 다음 silicon과 software coverage를 내지 못하면 단일 workload 우위가 platform update 한 번에 좁아질 수 있다.

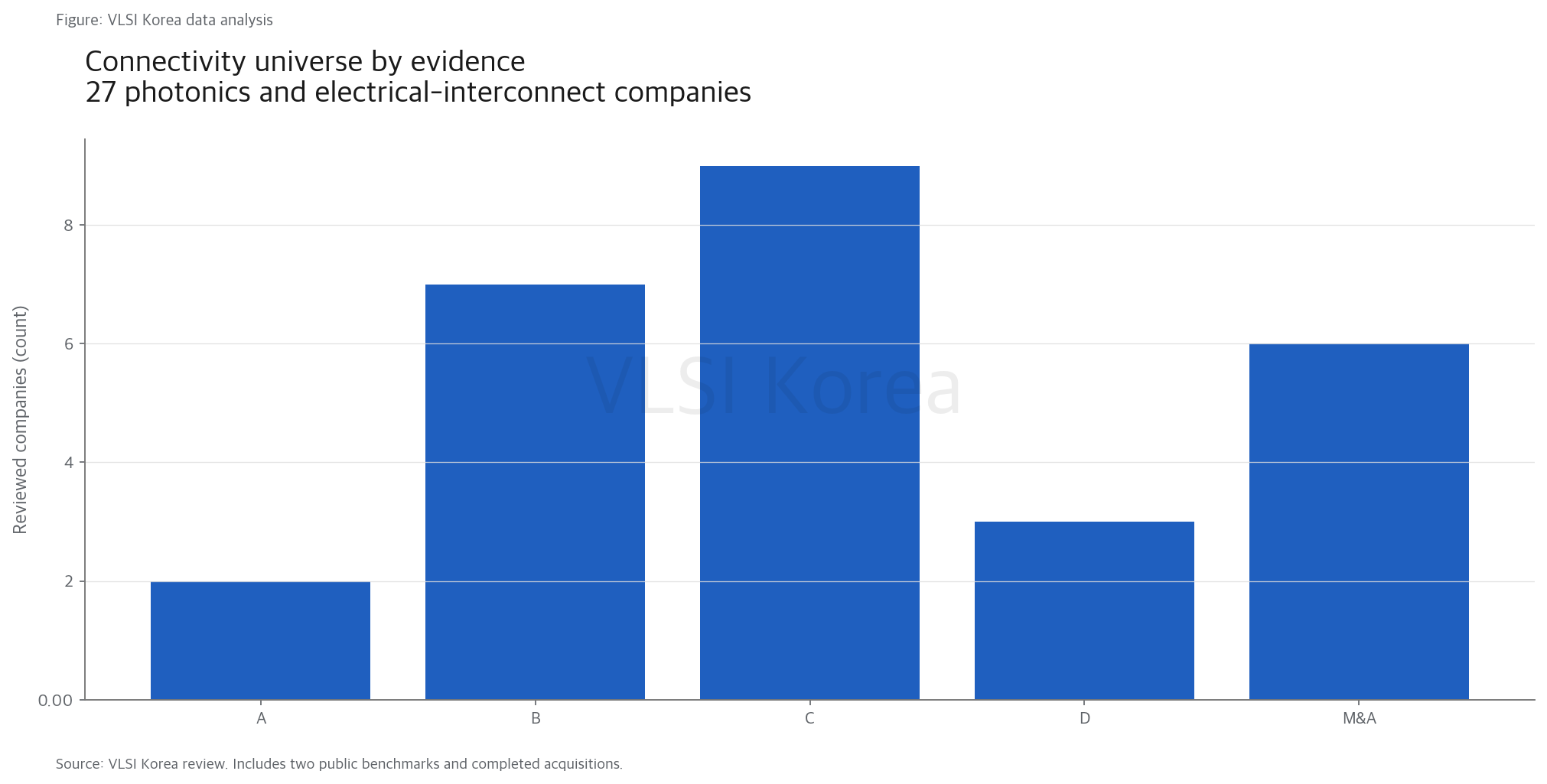

5. photonics·interconnect: 인수 가격보다 qualification이 해자다

읽는 법: 광이 빠르다는 물리학은 모두 안다. 누가 수율 좋게 붙이고, 시험하고, 고장 난 뒤 교체할 수 있는지가 사업 해자다.

Ayar Labs와 Lightmatter는 optical I/O를 package 가까이 끌어온다. Avicena와 Hyperlume은 수많은 microLED lane, Scintil과 Xscape는 laser integration, DustPhotonics와 Ranovus는 SiPh engine의 조립과 수율을 판다. 같은 photonics라도 moat의 위치가 modulator, laser, attach, package, switch, control software로 다르다.

전기식 interconnect도 남는다. Eliyan은 organic package die-to-die, XConn은 CXL switch, Enfabrica는 multi-protocol fabric, DreamBig은 chiplet building block, Cornelis와 Xsight는 scale-out network를 판다. 광과 구리는 승자독식 관계보다 거리·전력·serviceability에 따라 경계를 나눈다.

2025-2026년 M&A는 component layer의 전략가치를 보여준다. Marvell은 Celestial AI와 XConn을, Qualcomm은 Alphawave를, Ciena는 Nubis를, Credo는 Hyperlume을 흡수했다. 그러나 headline deal value는 startup revenue가 아니고, 인수 뒤 product roadmap과 customer ramp를 확인해야 한다.

상태 정정도 중요하다. Kandou는 2026년 독립 제품 활동이 확인되므로 인수됐다고 쓰면 안 된다. Enfabrica는 NVIDIA의 회사 인수 완료 발표가 아니라 license와 핵심팀 이동으로 보는 것이 맞고, 법인 존속·독립 roadmap·support capacity를 따로 검증해야 한다.

6. edge·sovereign: 낮은 전력보다 설치와 조달이 오래 남는다

읽는 법: edge에서는 최고 TOPS보다 fanless enclosure 안에서 센서부터 결과까지 예측 가능하게 끝내는 것이 해자다.

Hailo, SiMa.ai, Axelera AI, DEEPX, MemryX와 EdgeCortix의 경쟁은 데이터센터 benchmark 축소판이 아니며 camera pipeline, model compiler, host CPU 부담, thermal envelope, module supply와 OEM lifecycle가 함께 맞아야 한다. Innatera, SynSense, BrainChip, POLYN은 event-driven·neuromorphic 방식으로 always-on sensor의 좁은 전력대를 노린다.

자동차·robotics는 qualification과 distribution이 강하다. Horizon Robotics, Black Sesame, Uhnder, Inuitive와 Arbe는 sensor-to-output stack, vehicle program, safety·reliability와 긴 지원기간이 진입장벽이다. design win을 production vehicle shipment로 오인하지 않는 동시에, qualification data 자체가 다음 고객의 전환비용이 된다는 점도 봐야 한다.

sovereign AI의 해자는 국적이 아니다. Rebellions와 FuriosaAI는 한국 cloud·memory·foundry·system channel과 연결될 기회가 있지만, local procurement만으로 software coverage와 다음 silicon 비용이 해결되지는 않는다. 중국의 Cambricon, Moore Threads, MetaX, Biren, Enflame과 Iluvatar는 수출통제 아래 local stack과 조달을 빠르게 만들었지만 고객 집중과 공급 제약이라는 반대편 위험도 갖는다.

따라서 이 지도는 승자표가 아니다. A는 감사 증거가 많다는 뜻이지 성장이나 재무안전 보장이 아니며, Blaize처럼 A급 매출 증거와 going-concern 위험이 공존할 수 있다. B·C 기업도 특정 edge socket에서 더 강한 해자를 가질 수 있다.

실사 질문은 네 가지로 끝낼 수 있다. 지금 유료로 쓰는 named customer가 누구인지, 새 모델을 몇 주 안에 지원하는지, 다음 tape-out과 HBM·package 자금을 누가 대는지, incumbent가 같은 기능을 SKU나 library로 번들할 때 무엇이 남는지 묻는다.

Korean Lens - 한국 기업 입장

한국 기업에는 메모리와 제조 생태계가 자동 해자가 아니다. Rebellions와 FuriosaAI가 HBM·Samsung manufacturing·국내 cloud를 연결하고, DEEPX와 Mobilint가 module·산업 channel을 넓힐 때만 공급망이 switching cost로 변한다.

채용 관점에서는 architecture 팀보다 compiler·runtime, package·SI/PI, field application, customer success와 next-silicon program management의 지속성을 확인해야 한다. 회사가 이 역할에 반복 투자하는지가 단일 benchmark보다 생존 가능성을 더 잘 보여준다.

판단을 깨는 조건

- 2027년까지 C·D급 기업 다수가 named production customer와 반복 매출을 공개하고 GPU 대비 software migration 비용도 낮게 유지한다면 공개 증거와 해자 사이의 보수적 구분은 지나치게 엄격했던 셈이다.

- NVIDIA·AMD와 hyperscaler가 optical I/O, in-memory compute, edge compiler, sovereign support를 18개월 안에 제품군으로 흡수해 startup의 고객 유지율을 급격히 낮추면 component-layer 해자 가설이 약해진다.

- 인수된 기술이 인수자 안에서 roadmap·매출로 전환되지 않고 반복적으로 중단된다면 M&A를 기술가치 회수 경로로 보는 해석도 낮춰야 한다.

다음 관찰 일정

- 2026-Q4: Etched Sohu, Taalas HC1, Fractile과 VSORA의 independent benchmark·board·rack milestone

- 2027-H1: Rebellions REBEL, FuriosaAI RNGD, Positron Asimov의 양산·named deployment·반복 주문

- 2027-H2: Lightmatter Passage, Ayar TeraPHY, Avicena LightBundle의 production qualification과 package yield

- 2027-FY: Cambricon·중국 GPU 상장사의 고객 집중, gross margin, supply continuity와 해외 매출 변화

Sources

- Cerebras Systems - Q1 2026 Form 10-Q and IPO completion (2026-05-20)

- Groq - NVIDIA non-exclusive inference license (2025-12-24)

- Rebellions - $400 million pre-IPO and RebelRack/RebelPOD (2026-03-30)

- FuriosaAI - RNGD product (accessed 2026-07-17)

- Marvell - Q1 FY2027 Form 10-Q (2026-06-05)

- Qualcomm - Alphawave Semi acquisition completed (2025-12-18)

- NXP - Aviva Links and Kinara acquisitions completed (2025-10-27)

- Graphcore - Group tax strategy (accessed 2026-07-17)

- Untether AI - transaction with AMD (2025-06-05)

- Arm - Q4 FYE26 results (2026-05-06)

- Cambricon - 2025 annual report (2026-03-12)

- Innatera - Pulsar at Embedded World 2026 (2026-03-10)